In today’s fast-paced world, financial literacy is more important than ever. Many of us were never taught about financial planning in school or by our parents, leaving us vulnerable to financial crises. If you’re one emergency away from bankruptcy, it’s time to take control of your finances. Here’s a straightforward guide to help you start your financial planning journey.

Step 1: Get Term Insurance

The first step in securing your family’s future is to get a term insurance policy. This is a cost-effective way to ensure that your loved ones are protected financially if something happens to you.

How Much Coverage Do You Need?

Use this formula to determine your total sum assured:

Total Sum Assured = ((Total Monthly Spend + EMI) / 50,000) * 1 Crore

This calculation ensures that your family can maintain their lifestyle even in your absence. Remember, you can discontinue this insurance once you have built a substantial financial cushion.

Step 2: Invest in Health Insurance

Medical emergencies can drain your savings faster than you think. A good health insurance policy protects you from unexpected medical expenses, allowing you to focus on growing your wealth.

Coverage Recommendations:

For Parents: At least ₹10 Lakhs per person.

For Yourself, Spouse, and Children: At least ₹5 Lakhs per person.

Don’t rely solely on employer-provided insurance. Create your own policy to avoid complications related to pre-existing conditions or waiting periods when switching jobs.

Step 3: Save Before You Spend

One of the simplest yet most effective financial habits is to save before you spend. Here’s how:

Open Two Bank Accounts:

Salary Account: Where your paycheck goes.

Savings Account: Transfer the necessary amount for EMIs and savings as soon as you receive your salary.

Spend What’s Left: Use the remaining balance in your salary account for your daily expenses. This method ensures that you prioritize savings and debt repayment.

Step 4: Plan for Retirement

A common rule of thumb is that for every ₹50,000 you need per month today, you will need ₹1 Crore at retirement. However, if you wish to maintain your current lifestyle, consider planning for ₹2 Crores for every ₹50,000.

Why the Increase?

As you age, your lifestyle may change, and inflation will affect your purchasing power. Observing your parents and in-laws can provide insight into the financial needs of retirement.

Step 5: The 15-15-15 Rule for Investing

Investing is crucial for building wealth. Here’s a simple rule to follow:

Invest ₹15,000 every month for 15 years.

Aim for a growth rate of 15% per annum.

By following this strategy, you could accumulate ₹1 Crore by the end of the investment period. Adjust your monthly investment based on your retirement goals and the number of Crores you need.

Where to Invest?

Achieving a 15% return is challenging but possible through well-researched mutual funds or direct equity investments. If you’re unsure, consider investing in index funds, which can provide a more conservative return of around 12%.

Conclusion

Financial planning may seem daunting, but taking these steps can help you secure your future and that of your family. Remember, I am not a certified financial planner or investment advisor; I am simply sharing lessons I’ve learned and practiced over time for educational purposes. Start your journey today, and take control of your financial destiny!

Here’s the Comprehensive List of Our Blogs: Keep it Handy, Share with Friends and Family, Smash that Like Button, and Subscribe to Receive Blog Updates First. Your support fuels our passion for creating insightful content!

Charlie Munger, the esteemed investor and vice chairman of Berkshire Hathaway, is often celebrated for his remarkable intellect, his partnership with Warren Buffett, and his invaluable insights into finance and life. However, behind his towering success lies a story marked by adversity, resilience, and personal challenges that shaped his journey in profound ways.

Born into a family grappling with financial hardship during the Great Depression, Munger’s early years were defined by struggle. The economic turmoil of the era, coupled with his father’s health issues, imbued him with a deep appreciation for resilience and resourcefulness from a tender age. These formative experiences laid the groundwork for the principles that would guide him through life’s trials and triumphs. Yet, Munger’s path to success was fraught with personal tragedies. In 1953, he experienced the devastating loss of his eldest son, Teddy, to leukemia—an unimaginable blow that left an indelible mark on his family. Despite grappling with profound grief, Munger found the strength to persevere, drawing on the resilience instilled in him by his upbringing.

In the realm of personal relationships, Munger also faced challenges. His first marriage ended in divorce, a painful chapter in his life that tested his resolve and resilience. However, even in the face of heartbreak, Munger remained steadfast in his commitment to personal growth and self-improvement.

These trials and tribulations, though deeply personal, played a pivotal role in shaping Munger’s worldview and approach to life. From the crucible of adversity emerged a man of extraordinary wisdom, empathy, and compassion—a beacon of inspiration for generations to come.

Top 5 Personal Finance lesson I learnt from Charlie Munger.

The Power of Compound Interest: Munger famously said, “Understanding both the power of compound interest and the difficulty of getting it is the heart and soul of understanding a lot of things.” Explore how individuals can harness the power of compound interest by starting early, staying invested, and avoiding unnecessary debt. Provide practical tips on how to leverage this concept to build long-term wealth.

Seeking Knowledge from Diverse Disciplines: Munger is known for his multidisciplinary approach to problem-solving. Discuss the importance of continuously expanding one’s financial literacy by learning from various fields such as psychology, history, and economics. Offer reading recommendations and online resources that can broaden readers’ perspectives and improve their decision-making skills.

Value Investing Principles Applied to Personal Finance: Munger and Buffett’s investment philosophy revolves around the principles of value investing. Explore how individuals can apply these principles to their personal finances by focusing on buying quality assets at reasonable prices, avoiding speculative investments, and maintaining a long-term perspective. Provide practical examples of how to assess the intrinsic value of assets and make informed financial decisions.

The Importance of Frugality and Delayed Gratification: Munger advocates for frugality and delayed gratification as essential virtues for financial success. Discuss strategies for living below one’s means, distinguishing between wants and needs, and cultivating patience when it comes to spending and investing. Share real-life anecdotes of individuals who achieved financial independence by practicing these principles.

Risk Management and Decision-Making: Munger emphasizes the importance of understanding and managing risk in both investing and life. Explore strategies for assessing and mitigating financial risks, such as diversification, asset allocation, and maintaining an emergency fund. Discuss the role of rational decision-making in financial planning and how to avoid common cognitive biases that can lead to costly mistakes.

Charlie Munger’s timeless wisdom offers invaluable insights for mastering personal finance. By adopting principles such as compound interest, continuous learning, value investing, frugality, and risk management, individuals can take control of their financial future and work towards achieving their long-term goals. As Munger famously said, “The best thing a human being can do is to help another human being know more.” Let’s continue to learn and grow together on our journey to financial well-being.

Here’s the Comprehensive List of Our Blogs: Keep it Handy, Share with Friends and Family, Smash that Like Button, and Subscribe to Receive Blog Updates First. Your support fuels our passion for creating insightful content!

Disclaimer: This blog post is intended for informational purposes only and should not be considered as financial advice. Always conduct thorough research and consult with a qualified financial professional before making investment decision.

Growing up, I was fortunate to have parents and relatives who instilled in me the value of saving and equipped me with the tools to do so. Their guidance not only shaped my financial habits but also spared me from the precarious hand-to-mouth existence that many find themselves in month after month. Reflecting on this, I can’t help but feel immensely fortunate.

Yet, I also find myself pondering a perplexing question: why aren’t such fundamental life skills taught in schools? In a country like India, discussions about money are often treated as taboo subjects in educational institutions. Whether this omission is unintentional or deliberate is a matter open to debate. Perhaps it stems from a desire to foster a spending-driven economy, one that prioritizes showcasing GDP growth and economic prowess to the world.

Regardless of the reasons behind this educational gap, I’ve made a personal commitment to ensure that my child, and anyone else willing to listen, receives the financial education that our schooling system overlooks. Through this blog, I aim to share the framework that I believe is the cornerstone of a solid financial education for children.

This framework, inspired by the teachings of my grandparents, parents, and countless books on personal finance, serves as a blueprint for nurturing financial literacy from a young age. By summarizing and elucidating this framework here, my hope is that readers—parents like myself, who may have felt unequipped to tackle this subject—can adapt it to their own needs and set their children on a path towards financial empowerment. Join me as we embark on this journey to equip the next generation with the tools they need to navigate the complexities of personal finance with confidence and competence.

Step 1 : Introduce a Personalised Piggy Banks at Age 3.

At the age of 3 or so, gift your child a piggy bank that is visually appealing and engaging to them, not just what the parents prefer. Choose a piggy bank design that aligns with your child’s interests and personality, whether it’s a favorite cartoon character, animal, or vibrant color. Making the piggy bank personalized and fun will help spark their interest in saving money from an early age. This hands-on tool can serve as the foundation for teaching basic financial concepts through interactive play and setting savings goals. Starting with a piggy bank they genuinely enjoy using can make the process of learning about money management more enjoyable and impactful for young children.

To instill the habit of saving in your child, regularly give them any spare coins or small denomination notes to deposit into their piggy bank. Encourage them by explaining that once the piggy bank is full, they can use the saved money to buy something they truly desire. When your child requests a toy or item, teach them patience by suggesting they wait until the piggy bank is full to make the purchase with their own savings. Additionally, on days when your child displays exceptional behavior, reward them with a little extra money to add to their savings, reinforcing the connection between good behavior and positive outcomes. This approach not only teaches financial responsibility but also cultivates patience, delayed gratification, and the value of hard-earned money in a practical and rewarding manner.

As your child’s piggy bank starts to fill up with savings, make it a point to involve them in your regular shopping trips. When you go to the supermarket or other stores, hand the money over to your child and have them pay the merchant directly. This hands-on experience allows them to see the process of exchanging money for goods and services. Once you get home, take the time to discuss the event with your child. Help them understand that money is required to purchase the items you need, reinforcing the connection between saving, spending, and obtaining the things you want or require. This real-world practice, combined with the follow-up conversation, can solidify your child’s grasp of basic financial concepts in a meaningful, engaging way.

Make it a point that kid gets a chance to buy what ever it wants with very limited or no restrictions.

Step 2 : Introducing the ‘Co-Pay Model’: Teaching Kids Financial Responsibility Through Shared Costs at Age 5.

When your child reaches the age of 5, consider transitioning from a full-pay model to a cost-sharing approach for purchases. Whenever your child requests a toy or other item, ask them to contribute 5-10% of the cost from their piggy bank savings. This teaches them the value of money and the importance of prioritizing their spending. Reinforce the lesson by refusing to buy the item if their piggy bank is empty, encouraging them to save up for the desired purchase.

At the same time, avoid over-gifting money to your child. Instead, provide additional funds as rewards for positive behaviors, such as helping to clean their room, making their bed, or going a day without screen time. This ties financial rewards to good habits, further instilling the connection between responsible actions and financial benefits. By transitioning to a cost-sharing model and selectively rewarding desired behaviors, you can continue building your child’s financial literacy and money management skills as they grow older.

In the copay model of teaching delayed gratification to children, it is essential to emphasize the importance of delayed gratification in relation to the size of the purchase. By linking the copay percentage to the ticket size of the item they desire, children can better grasp the concept of delayed gratification. When the copay percentage increases with larger purchases, children learn that patience and saving are required for more significant rewards. This approach not only reinforces the value of self-control and discipline but also teaches children the correlation between delayed gratification and achieving more substantial goals. By adjusting the copay percentage based on the cost of the desired item, kids can develop a deeper understanding of delayed gratification and the rewards that come with patience and long-term planning.

Step 3 : Bring out the little Entrepreneur at Age 8.

Encouraging children to develop new skills and turn them into products or services they can sell is a powerful way to build their financial literacy and entrepreneurial mindset. This approach aligns with the philosophy espoused by Naval Ravikant – “Learn to Sell, Learn to Build. If you can do both, you will be unstoppable.”

Start by helping your child identify their interests and talents. Perhaps they enjoy making colorful paintings or have a knack for crafting homemade soaps. Provide them with the necessary resources and guidance to turn these hobbies into small business ventures. Teach them how to source materials, create their products, and market them to friends, family, and the local community.Leverage online resources to inspire your child and provide them with ideas.

Explore stories of other smart, young entrepreneurs who have found success through their creativity and determination. This exposure can spark their imagination and motivate them to think beyond traditional ways of earning money and save them in the piggy bank and involve in the co-pay model.

Encourage your child to experiment, learn from failures, and continuously iterate on their business ideas.By empowering your child to become a young entrepreneur, you are not only fostering their financial literacy but also instilling valuable skills such as problem-solving, critical thinking, and the ability to turn their passions into profitable ventures. This holistic approach to personal finance education can set your child up for long-term success, both financially and in their overall personal development.

Step 4 : Transitioning from Piggy Bank to Formal Banking at Age 12.

As your child’s savings in the piggy bank grow, it’s time to introduce them to the formal banking system. Open a bank account in their name and transfer the accumulated funds from the piggy bank. Take your child to the bank counter and have them personally hand over the money to the teller for deposit. This hands-on experience will help them understand the process of depositing funds into a bank account.

Explain the entries made in the passbook, showcasing the balance and any deposits made. When it’s time to make a withdrawal, repeat the process, allowing your child to interact with the teller and observe the updated balance. Emphasize the importance of this record-keeping, as it helps them track their savings.

As your child begins to deposit their savings into a formal bank account, introduce them to the concept of interest. Explain that the bank pays them a small percentage, known as interest, for keeping their money in the account. This interest is credited to their account on a regular basis, typically monthly or quarterly.Encourage your child to closely monitor the “Interest” line item in their passbook.

Explain the simple interest calculation, where the interest earned is a function of the principal amount, the interest rate, and the time period. Invite them to calculate the interest themselves, fostering a deeper understanding of how their savings can grow over time.Furthermore, discuss the bank’s perspective – how they utilize the deposited funds to generate their own revenue, and why they are willing to share a portion of that with account holders in the form of interest. This will help your child appreciate the mutually beneficial relationship between the bank and the account holder, setting the stage for more advanced financial concepts in the future.

After your child has become comfortable with the basic savings account, introduce them to more advanced banking products like recurring deposits (RDs) and fixed deposits (FDs). Explain that an RD allows them to set aside a fixed amount of money at regular intervals, typically monthly, to grow their savings systematically.Guide your child through the process of opening an RD account, emphasizing the importance of consistent contributions. Demonstrate how the interest earned on an RD is typically higher than a regular savings account, rewarding their disciplined saving habits. As the RD matures, have your child withdraw the funds and observe the total amount, including the interest earned.

Building on this experience, introduce the concept of a fixed deposit (FD). Explain that an FD allows them to deposit a lump sum of money for a predetermined period, usually ranging from a few months to several years. Highlight how FDs generally offer even higher interest rates compared to RDs, as the bank can rely on the funds being unavailable for a longer duration. Encourage your child to allocate a portion of their savings into an FD, reinforcing the idea of diversifying their financial portfolio.

By guiding your child through the transition from a basic savings account to more sophisticated banking products, you are equipping them with a comprehensive understanding of how to grow their wealth through various savings and investment strategies.

Summary :

In this blog post, we explored a comprehensive approach to teaching kids about personal finance, starting from a young age with the introduction of a piggy bank and gradually transitioning to formal banking. By involving children in real-world transactions, encouraging savings, and introducing them to banking products like recurring deposits and fixed deposits, parents can instill valuable financial literacy skills and cultivate an entrepreneurial mindset in their children. Understanding the concepts of interest, delayed gratification, and the importance of consistent saving lays a strong foundation for children to make informed financial decisions and build a secure financial future.

Here’s the Comprehensive List of Our Blogs: Keep it Handy, Share with Friends and Family, Smash that Like Button, and Subscribe to Receive Blog Updates First. Your support fuels our passion for creating insightful content!

Disclaimer: This blog post is intended for informational purposes only and should not be considered as financial advice. Always conduct thorough research and consult with a qualified financial professional before making investment decision.

Unveiling the Art of Stock Investing: Expertise, Dedication, and the Gift of Time

Delving into the world of stock investing requires a blend of expertise, dedication, and a generous investment of time. Firstly, becoming adept at analyzing businesses is akin to becoming a detective. It involves scrutinizing a company’s financial statements – the balance sheet, income statement, and cash flow statement – to understand its health. This financial sleuthing also extends to assessing a company’s growth potential, competitive positioning, and the broader sector trends in which it operates. This expertise doesn’t happen overnight; it’s a continuous learning process.

Dedication is the backbone of successful investing. Monitoring the stock market demands a commitment to staying informed about global and industry-specific news, economic changes, and shifts in market sentiment. Understanding the intricacies of financial markets and developing a keen sense for when to act or hold requires persistent effort.

Time is the unsung hero of the investing journey. Just as Rome wasn’t built in a day, a well-constructed stock portfolio takes time to evolve. Patience is crucial, as markets can be unpredictable in the short term. Regularly reviewing and adjusting your investment strategy, and being prepared for the long haul, is part of the time investment required.

In essence, becoming a savvy stock investor is not just about buying and selling; it’s about honing analytical skills, staying dedicated to the market’s pulse, and giving investments the time they need to flourish. This trio of expertise, dedication, and time is the winning combination for those navigating the exciting yet complex world of stock investing.

Simplicity in Diversity: The Effortless Journey of Investing in Mutual Funds

Investing in mutual funds offers a straightforward and user-friendly path for those seeking a hands-off approach to building wealth. The process begins with selecting a mutual fund that aligns with your financial goals, time horizon, and risk tolerance. Unlike scrutinizing individual stocks, this involves evaluating the fund’s historical performance, expense ratio, and the expertise of the fund manager. Effort is considerably reduced as you’re essentially placing your trust in the hands of experienced professionals who manage the fund’s portfolio.

Once the choice is made, purchasing mutual fund shares is a breeze, often just a few clicks away through an online platform or with the assistance of a financial advisor. The beauty of mutual funds lies in their inherent diversification – your investment is spread across a variety of assets, reducing the impact of a poor-performing individual investment.

Tracking a mutual fund is simpler compared to managing a portfolio of individual stocks. Regular updates on the fund’s performance are readily available, allowing investors to gauge how well it aligns with their objectives. The fund manager takes on the responsibility of adjusting the portfolio to maximize returns within the fund’s defined strategy.

Selling mutual fund shares is also uncomplicated. Investors can redeem their shares at the current net asset value (NAV), providing liquidity and flexibility. The exit decision is often tied to changes in your financial goals, time horizon, or risk tolerance.

The icing on the cake is having an experienced fund manager at the helm, making tactical decisions on behalf of investors. Despite the expertise involved, mutual funds typically charge a modest management fee, allowing investors to benefit from professional management while keeping costs reasonable. In essence, investing in mutual funds offers a hassle-free experience, combining the simplicity of the process with the expertise of a seasoned fund manager to navigate the financial markets on your behalf.

You can read more about Mutual Funds here and then here

Why I choose Direct Stock Investing over Mutual Funds and why I don’t blindly recommend my approach for all ?

Certainly! Here’s a refined version of your idea with improved grammar, sentence formation, and spelling:

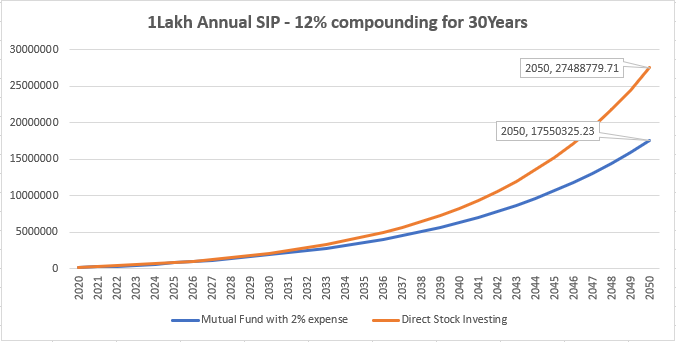

Upon analyzing the financial landscape, a compelling argument surfaces in the realm of investment strategies. Consider a scenario where one invests directly in stocks, allocating 1 lakh per year for 30 years, with an assumed annual growth rate of 12%. The outcome is a substantial 2.7 Crores at the end of the period. Contrastingly, envision investing in a mutual fund, maneuvering through various funds while maintaining the same growth rate of 12%. However, factor in the 2% annual toll for entry criteria, expense ratio, and exit load to the mutual fund house. The result? A take-home amount of 1.7 Crores, marking a staggering loss of over 1 Crore, translating to nearly a 30% deficit.

While one might argue that transaction frequency might be lower or the charges could be less than the stipulated 2%, the counterargument asserts that diligent analysis can potentially yield more substantial returns in direct stock investing. The crux of the debate lies in the significance of a 30% surplus post 30 years versus the present commitment of time and effort required for understanding, investing, and tracking.

For individuals like me who are coming from a lower-middle-class background, the prospect of 30% additional funds after three decades holds paramount importance. It not only secures financial stability but also offers a competitive advantage. The time spent from in-depth financial analysis can be redirected towards self-improvement in diverse areas such as economics, geopolitics, resource optimization, and leadership skills. This multifaceted skill set can contribute to career growth, potentially leading to increased income. With the newfound financial flexibility, one could even enhance their SIP contributions over the years, generating substantial returns upon retirement.

However, it’s crucial to acknowledge that this perspective may not resonate universally. Individuals who prioritize present-day time constraints, value simplicity, and are uninterested in delving into the complexities of business analysis may find comfort in the ease of mutual fund investments. The choice between direct stock investments and mutual funds ultimately hinges on personal preferences, financial goals, and the perceived trade-off between immediate convenience and long-term financial gains.

Here’s the Comprehensive List of Our Blogs: Keep it Handy, Share with Friends and Family, Smash that Like Button, and Subscribe to Receive Blog Updates First. Your support fuels our passion for creating insightful content!

Disclaimer: This blog post is intended for informational purposes only and should not be considered as financial advice. Always conduct thorough research and consult with a qualified financial professional before making investment decision.

Are you curious to discover the key principles that have steered my financial journey towards success? In this blog post, I’m not here to offer advice, but rather to share three golden rules that have personally guided my investments and contributed to my financial well-being. These rules have stood the test of time and have proven effective for me. I’m excited to share them with you, so you can incorporate them into your own investment strategy, keeping things straightforward and appealing.

1. Rule of Profit Potential

Have you ever wondered what lies at the heart of every successful business venture? Well, it’s not magic, but a powerful equation that can transform your understanding of profit generation. Let’s delve into the Profit Equation. It’s a key piece of knowledge that every business owner should have in their toolkit.

P = Q * (S-C) —- (Profit Equation)

Now, let’s break it down. P represents the profit in any given year, Q is the number of units of products sold, S stands for the selling price of those products, and C represents the cost at which the products were acquired or made by the company. In simple terms, this equation tells the story of how your business can turn a profit.

Imagine you’re in the business of selling apples. If you buy apples for 50 Rs each, sell them at 100 Rs each, and manage to sell 20 apples in a year, your profit can be calculated as follows: Profit = 20 * (100 – 50) = 1000 Rs for the year.

Here is a concise summary of the key factors that i consider in the context of the profit equation:

Product Relevance: Ensure that the company’s products remain in demand and relevant for the long term, securing a steady/growing consumer base.

Innovative Growth: Look for efforts to increase sales (Q) through product innovation / Quality and by adding unique value to the product, which can subsequently boost profits.

Cost Optimization: Evaluate the company’s strategies for reducing production or purchase costs (C) through wise capital allocation in to efficient machines , adapting supply chains, Training the labor etc.

Pricing Power: Assess the company’s ability to adjust selling prices (S) when production or purchase costs (C) rise. This demonstrates pricing power and a potential competitive advantage in the market.

Thanks to my Grandfather who thought me this !

2. Rule of Credibility

One of my uncles started a clothing shop when I was 13-14 years old, and I asked him how he measured the success of his business. The answer he gave me has had a profound influence on me to this day, and I am confident it will serve as a guiding light for me and future generations. He said, ‘I will buy clothes worth 10 lakh rupees and I am certain I can make a monthly profit of 8,300 rupees, thus generating around 10% return on my investment. If I start making less, there’s no point in continuing because I could simply place that money in the bank as Fixed Deposit (FD), which would pay me 8% interest anyway. So, all he was concerned about was the right allocation of capital and targeting returns on his equity.”

ROE = LR * ATR * NPM —– (Return on Equity)

Although this equation may appear complex at first glance, it is relatively straightforward. A business can achieve a higher Return on Equity (ROE) by employing one or a combination of the following strategies:

1. LR – Leverage Ratio: This involves taking on leverage and using it wisely, often referred to as ‘good debt.’ For example, if my uncle’s shop is successful, even if he doesn’t have the necessary capital, banks would likely be willing to lend him 10 lakhs, which he could borrow at a 9% interest rate to establish a new shop in a neighboring town. If he can generate a 10% return from it, pay 9% to the bank, and enjoy the 1% difference as additional profits.

2. ATR – Asset Turnover Ratio: My uncle doesn’t need to utilize all his capital to achieve a 10k monthly profit. He can optimize his inventory over time by learning about customer tastes, preferences, and seasonal trends. By keeping only 4-5 lakhs worth of clothing in stock at any given time and investing the rest in fixed deposits (FDs) at the bank, he can generate additional returns. This, of course, requires time and market insight to achieve.

3. NPM – Net Profit Margin: This can be a bit challenging to achieve. Instead of buying clothing from the same vendor, my uncle can explore alternative suppliers who offer a limited range at a lower cost. However, he must tread carefully, as this could potentially impact sales if customers seek a wider variety or the latest fashion trends. Alternatively, he might consider increasing the selling price, but this would require a unique selling proposition or a near-monopoly in the town.”

After witnessing my uncle’s success over the years, I couldn’t help but contemplate suggesting an alternative to borrowing money from the bank. Why not use my 10 lakhs to start another shop in a new town, with the aim of enjoying returns higher than what traditional FDs could offer? However, before making such a decision, I considered several factors carefully:

Town Selection: Is he choosing a town with significant potential for sales and growth?

Trustworthiness: Can I trust my uncle’s commitment to the business, especially in light of his past borrowing and repayment history with other individuals?

Equity Fairness: Is he treating me fairly as a minority shareholder in his business, ensuring that he doesn’t allocate excessive expenses for his personal gain, thus diminishing my returns?

These considerations mirror the questions we must ask ourselves before investing in a company in the stock market. Trust, potential for growth, and fairness are crucial aspects in both scenarios.

Thanks to my Uncle who thought me this !

3. Rule of Risk-Adjusted Returns

Although I understood how a business is created and executed, I did not have the right method for valuation. In fact, I didn’t even know what valuation was until I started investing in the stock market and buying shares in businesses.

Thanks to Ben Graham, Uncle Warren, and Aswath Damodaran, they have made a deep impact on my thinking when it comes to valuations. Ben Graham taught me what a margin of safety is, Uncle Warren taught me how to understand it along with the economy, and Aswath Damodaran taught me a whole host of things, including discounted cash flow, which is one of the primary tools I use today.

I promise to write a dedicated blog on valuation , describing it here will take a lot of space and doesn’t make the blog a pleasure to read

Here’s the Comprehensive List of Our Blogs: Keep it Handy, Share with Friends and Family, Smash that Like Button, and Subscribe to Receive Blog Updates First. Your support fuels our passion for creating insightful content!

Disclaimer: This blog post is intended for informational purposes only and should not be considered as financial advice. Always conduct thorough research and consult with a qualified financial professional before making investment decision.

Introduction: The Importance of Tracking Returns for Financial Success.

Investing wisely is a key aspect of personal finance, but it’s equally vital to track and understand the returns on your investments. This tracking provides valuable insights into the growth of our wealth and helps us make informed financial decisions. In this guide, we’ll explore two essential tools for measuring returns: CAGR (Compound Annual Growth Rate) for lump-sum investments and XIRR (Extended Internal Rate of Return) for periodic investments. With a firm grasp of these concepts, we’ll be better equipped to navigate the world of personal finance and investing.

CAGR (Compound Annual Growth Rate): Calculating Returns for Lumpsum Investments.

Let’s start with CAGR, a fundamental metric for evaluating the performance of a lumpsum investment over a specific period. Imagine you invested a sum of money, say $10,000, in a stock portfolio a decade ago. Now, you want to know how well your investment has performed. CAGR comes to the rescue. It calculates the average annual growth rate of your investment, smoothing out the volatility of the market.

CAGR = ((EV/BV)^(1/n)) -1

Where:

EV is the Ending Value of the investment.

BV is the Beginning Value

n is the number of compounding periods (in years).

By applying the CAGR formula, you can determine the average annual growth rate of your investment. This empowers you to make informed decisions based on your investment’s historical performance.

Let’s calculate CAGR using an example:

Suppose you invested Rs 10,000 in a stock portfolio in 2013, and it grew to Rs 18,000 in 2023.

Year

Investment Value (Rs)

2013

Rs 10,000

2023

Rs 18,000

BV (Beginning Value) = Rs 10,000

EV (Ending Value) = Rs 18,000

n (Number of years) = 2023 – 2013 = 10

Using the CAGR formula:

CAGR=(18,000/10,000)^(1/10)−1

= 0.06447 { or } 6.45%

So, the CAGR for your investment over the ten-year period is approximately 6.45%.

Unlocking Wealth with XIRR: Evaluating Periodic Investments.

Now, let’s shift our focus to XIRR, a tool essential for analyzing periodic investments. Imagine you’re contributing varying amounts to your retirement fund each year for ten years. XIRR helps you calculate the annualized rate of return on this irregular investment pattern, providing a more accurate picture of your wealth’s growth.

Let’s consider an example where you make periodic investments in a retirement fund:

Year

Investment Amount (Rs)

2013

Rs 5,000

2014

Rs 6,000

2015

Rs 7,500

…

…

2022

Rs 12,000

To calculate the XIRR, you would use a spreadsheet software like Excel. Here’s how you would set it up:

In an Excel worksheet, list the years in column A and the investment amounts in column B.

In a cell, use the formula =XIRR(B2:B11, A2:A11). This calculates the XIRR for the given investments over the respective years.

Using this formula in Excel, you would find that the XIRR for this periodic investment pattern is approximately 8.72%.( Assumption)

Excel Guide to use XIRR formulae can be found here.

Conclusion: Empowering Your Financial Journey.

In conclusion, tracking our investment returns through CAGR and XIRR is paramount in achieving our financial goals. Whether you’re making lump sum investments or contributing periodically, these tools offer valuable insights into your wealth’s growth. With the knowledge gained from this guide, we’ll not only be equipped to make informed financial decisions but also have the tools to create our own financial tracking system in Excel. So, lets take charge of our financial future and watch your wealth grow!

Summary.

In this comprehensive guide, we delved into the significance of tracking investment returns in personal finance. We demystified the concepts of CAGR and XIRR, providing real-world examples and tables for better understanding. Additionally, we empowered you with the knowledge to develop your own Excel tools for calculating these essential metrics. By mastering CAGR and XIRR, you’ll have the insights and tools needed to make informed financial decisions and achieve your wealth-building goals. So, embark on your financial journey with confidence and watch your investments flourish.

Here’s the Comprehensive List of Our Blogs: Keep it Handy, Share with Friends and Family, Smash that Like Button, and Subscribe to Receive Blog Updates First. Your support fuels our passion for creating insightful content!

Disclaimer: This blog post is intended for informational purposes only and should not be considered as financial advice. Always conduct thorough research and consult with a qualified financial professional before making investment decision.

Introduction: Lost in the Race, Forgotten ‘Enough’.

In the relentless pursuit of wealth, we find ourselves caught in the rat race, often forgetting to pause and ask a fundamental question: how much is truly enough? Reflecting on my own journey, I recall that as a child, I believed having 10 lakhs would make life heavenly. However, with time, my aspirations escalated; from dreaming of 1 crore, I eventually aimed for 100 crores, influenced by societal notions of luxury. Reading “The Psychology of Money” by Morgan Housel unveiled a universal truth – this desire for more is an endless cycle. Even the wealthy yearn for greater wealth: Michael Jordan eyes Jeff Bezos, and Bezos eyes Elon Musk.

In a moment of contemplation, a lingering question emerged within me: “What is the threshold of sufficiency?” Turning to the wisdom of my guru, Acharya Chanakya, I discovered his profound insight: “

the moist important thing for a happy life is satisfaction. If you are satisfied with life then there will be no problem in your life.”To be satisfied , one must know how to control his senses. No one is happier than the person who is satisfied by controlling his senses.”

Thus began my quest to explore the concept of “enough.”

The Cost of Chasing More: Tragedies Unveiled.

Conversations with my friends opened my eyes to some harsh realities. One friend had spent ten years building up money, but lost it all in just a few months by trading in ways that were very risky. He was convinced by his colleagues that he could make more money quickly by trading instead of saving for a small piece of land.

Another friend shared that their family ran a chit fund, but things went wrong and they lost all the money they were taking care of for others. This led them to bankruptcy.

While growing up, I saw many people from lower middle-class families lose everything because they hoped to get rich quickly. They gambled all their money, even the little they had, just to avoid the shame of being broke.

My own family also struggled with money. We had times when we had to walk a long way to save a small amount of money, just to buy a simple snack.

Seeing all of these situations shaped how I handle money. It made me wonder: Is it really worth it to chase after money so much that we lose out on life, time for ourselves, and our self-respect?.

Purpose and Passion: The Dual Pathways of Life.

As we progress through life, our selection of business or profession naturally transforms. For certain individuals, their work becomes a channel through which they find a profound sense of purpose and fulfillment. However, contrasting this, there are those who find themselves trapped in roles that bring about dissatisfaction and resentment.

Irrespective of the specific circumstances, the notion of constructing a financial corpus gains paramount importance. This corpus serves as a reservoir of financial resources, a reservoir that is integral to attaining a state of financial independence. This state liberates individuals from the compulsion to work solely for monetary gain, thereby affording them the luxury to delve into their passions and interests with unbridled enthusiasm.

In essence, the strategic accumulation of wealth doesn’t solely cater to material acquisitions, but rather, it acts as a conduit to a more profound form of freedom. This freedom extends beyond merely quitting a disliked job; it empowers one to explore their innate potential, nurture their creative endeavors, and lead a life aligned with their true aspirations.

Unleashing the Potential: The Miraculous 2 Crore Corpus.

Let’s consider a scenario where an individual, through ethical means, manages to accumulate 2 crores in their business or profession. Imagine this sum being invested in an Indian index fund, which hypothetically yields a 9% year-on-year return (being conservative here, considering that historically NIFTY has averaged 12%). Suppose this person withdraws 1 lakh every month for 30 years, allowing the remainder to continue compounding. Surprisingly, at the end of these 30 years, the corpus would still amount to a substantial 10 crores!

This prompts us to question: do we truly require such a substantial amount of money? With age, our need for extravagant luxury often diminishes. By having comprehensive health insurance in place, monthly expenses could be significantly reduced.

After conducting this thought experiment, I found myself taken aback and pushed to delve deeper. Could I realistically aim to amass 2 crores and attain a form of financial independence? Certainly, this wouldn’t imply ceasing work, but rather, it would infuse a heightened sense of confidence and contentment into life. Wouldn’t that be a valuable achievement?

I’m not certain if 2 crores is “The” figure that applies to me. What I wish to emphasize to the reader is that each individual should take a pen and paper to ascertain this number. Without doing so, breaking free from the rat race can seem nearly impossible.

Upon reaching the juncture where our accumulated corpus is capable of consistently generating the desired monthly revenue while also undergoing substantial compounding, a pivotal decision arises. This crossroads invites us to consider bidding farewell to the professions that evoke our disdain or the jobs that no longer kindle our interest. The financial security provided by the self-sustaining corpus can empower us to relinquish roles that once held us captive in the pursuit of monetary gains, paving the way for new chapters aligned with our genuine passions and aspirations. This transition signifies a transformative shift from obligation to choice, from the compulsion of necessity to the liberation of fulfillment.

Dharma’s Light: Transforming Desires into Destiny.

Here come the natural question how do i find my passion?

Well its not that easy to answer , but not difficult either …

I can only quote some awakening links from the Sanathana Dharma.

Dharma is your unique purpose in life. It is the process by which you use your unique skills and passions to serve your community and the world.

There is a phrase in the Upanishads, one of the great Indian texts, that says:

” You are what your deepest desire is,

As is your desire, so is your intent,

As is your intent, so is your will,

As is your will, so is your deed,

As is your deed, so is your destiny. “

Wisdom from Mahabharata: Navigating the Battle Within for a Noble Life.

As we embark on the quest to discover a meaningful purpose for our lives, it’s crucial to bear in mind the insightful encapsulation of the Mahabharata by a wise individual:

“Mahabharata in a metaphorical way: the battle of Mahabharata is, actually, the battle between the good and evil present in ourselves; this means that we are composed out of forces of evil and of good. Our mental condition is not void: forces of evil and of good are present in us. Therefore, we cannot wait and see: we ought to take a decision on our moral constitution.”

Here’s the Comprehensive List of Our Blogs: Keep it Handy, Share with Friends and Family, Smash that Like Button, and Subscribe to Receive Blog Updates First. Your support fuels our passion for creating insightful content!

Disclaimer: This blog post is intended for informational purposes only and should not be considered as financial advice. Always conduct thorough research and consult with a qualified financial professional before making investment dec

Understanding Stock Movements: Long-Term Business Growth vs. Short-Term Speculation.

When it comes to stock movements, investors often witness two main driving forces: long-term business growth and short-term speculation. Business growth refers to the underlying performance of a company, including revenue growth, profitability, market share, and expansion plans. These factors influence the stock’s value over the long run and attract investors seeking sustainable returns.

On the other hand, short-term speculation is driven by market sentiments, news, rumors, or macroeconomic factors that cause rapid price fluctuations. Speculative investors aim to capitalize on short-lived price movements and often trade frequently based on these transient factors.

Understanding the distinction between these two forces is crucial for successful investing. Long-term investors focus on the fundamentals of the business, studying its competitive advantage, management team, industry trends, and growth potential. They ride the ups and downs, confident that the company’s strong fundamentals will drive the stock price over time.

Weathering the Storm: The Initial 5-10% Stock Dip.

One of the most nerve-wracking experiences for investors is witnessing their newly invested stock take a nosedive shortly after buying it. It’s essential to remember that the stock market is highly volatile and influenced by a myriad of factors, including investor emotions and speculative activities. A short-term dip in stock price doesn’t necessarily reflect the true value of the company or its long-term prospects.

To navigate these turbulent waters, investors must resist making impulsive decisions driven by fear and instead remain focused on their investment thesis. They should evaluate the reasons for the dip, discerning whether it’s related to business fundamentals or merely market sentiment. Often, such temporary declines present an excellent opportunity to accumulate more shares at a discounted price, amplifying future gains when the stock eventually rebounds.

The Long Horizon: The Importance of Conviction in Investing.

Investing with conviction means having complete faith in the companies you invest in and their long-term growth potential. Conviction-driven investors don’t panic during short-term market fluctuations because they have extensively researched the company’s financial health, competitive landscape, and management credibility.

When investors adopt a long-term perspective, they align their goals with the company’s growth trajectory, understanding that businesses experience ups and downs over time. Warren Buffet, one of the most successful investors, famously said, “Our favorite holding period is forever.” This approach emphasizes the value of patience, allowing the compounding effect to work its magic over extended periods.

Unveiling the Magic of Compounding Effect: A Tale of Two Investments with a small difference of returns per year.

A small investment of 15,000 INR per month consistently for 15 years in an asset that is generating 15% per annum would make one a “CROREPATI.” The key lies in selecting the right asset and staying the course consistently. Despite the investment being only around 27lakhs, the power of compounding and the choice of a high-yielding asset can lead to extraordinary wealth.

The only difference between Investment 1 and Investment 2 is the asset yield. In Investment 1, it was 15%, while in Investment 2, it was 14%. At first glance, this might seem like a small difference, but over the course of 10 years, it has made a significant impact, resulting in a difference of around 10lakhs in the final cumulative value. This underscores the remarkable effect even a slight variation in returns can have on long-term investments.

Embracing the Einstein Effect: The Power of Compound Interest.

Albert Einstein famously said, “Compound interest is the eighth wonder of the world. He who understands it, earns it … he who doesn’t … pays it.” This statement not only applies to financial investments but resonates in various aspects of life.

In conclusion, the path to financial success lies in embracing the power of patience and compounding in investing. By understanding the true drivers of stock movements, maintaining conviction in solid investments, and harnessing the magic of compounding, investors can unlock the full potential of their wealth. Remember, fortune favors the patient and disciplined, and the wonders of compounding can transform your financial journey into an extraordinary one.

Here’s the Comprehensive List of Our Blogs: Keep it Handy, Share with Friends and Family, Smash that Like Button, and Subscribe to Receive Blog Updates First. Your support fuels our passion for creating insightful content!

Disclaimer: This blog post is intended for informational purposes only and should not be considered as financial advice. Always conduct thorough research and consult with a qualified financial professional before making investment decision.

In 2008, Warren Buffet, the renowned investor and CEO of Berkshire Hathaway, issued a daring challenge to Ted Seides, a prominent hedge fund manager. Buffet offered Seides a staggering sum of 1 million USD and proposed a decade-long bet to determine which investment strategy would reign supreme: index investing or hedge funds. This captivating challenge was born out of Buffet’s strong belief in the merits of index investing and his desire to shed light on the often-controversial world of hedge funds.

Overview of Hedge Funds and Index Investing:

Hedge funds and index funds represent two distinct approaches to investing in the financial markets. Hedge funds are private investment funds managed by skilled professionals who aim to generate substantial returns for their clients. These managers often employ various strategies, including leveraging, which involves borrowing money to amplify potential returns. While leverage can magnify gains, it also significantly increases risk, potentially leading to substantial losses if the market moves against the fund’s positions. This approach can be appealing to some investors seeking higher returns, but it comes with higher levels of complexity and risk.

On the other hand, index investing, epitomized by funds that track well-established market indices like the S&P 500, adopts a more passive approach. Instead of attempting to beat the market, index investing seeks to replicate its performance, offering investors exposure to a diverse portfolio of stocks in proportion to their representation in the index. This strategy typically involves minimal leverage and lower costs compared to actively managed hedge funds.

It is important to note that while hedge funds are prevalent in many parts of the world, including the United States, they are not widely present in India due to regulations set by the Securities and Exchange Board of India (SEBI). SEBI has been cautious about allowing hedge funds in India due to concerns about increased risk and potential mismanagement of leverage, as well as the need to protect retail investors from complex and high-risk investment products.

The Decade-Long Battle: A Table of Results

Here’s a summary of the performance of Warren Buffet’s chosen S&P 500 index fund against the hedge fund managed by Ted Seides over the ten-year period:

Summary:

As the dust settled after ten years, Warren Buffet emerged victorious in his legendary wager against the hedge fund manager Ted Seides. The numbers showcased the undeniable power of patience and a long-term perspective in the stock market. Buffet’s index fund, with its steady and consistent growth, outperformed the more complex and actively managed hedge fund. This triumph aptly echoes Buffet’s timeless wisdom that the stock market is a mechanism for transferring wealth from the impatient to the patient, emphasizing the enduring value of index investing as a strategy for long-term success.

For More on Mutual Funds Read my Part 1 and Part 2 Blogs.

Here’s the Comprehensive List of Our Blogs: Keep it Handy, Share with Friends and Family, Smash that Like Button, and Subscribe to Receive Blog Updates First. Your support fuels our passion for creating insightful content!

Disclaimer: This blog post is intended for informational purposes only and should not be considered as financial advice. Always conduct thorough research and consult with a qualified financial professional before making investment decision.

Returns are the lifeblood of any financial endeavor, whether it’s personal finance or running a business. They represent the gains or losses generated from investments or operations over a specific period. In personal finance, returns are essential to measure the performance of investments, savings, and overall financial well-being. For businesses, returns play a crucial role in the Profit and Loss (PnL) statement, indicating how effectively the capital invested is being utilized to generate profits. Analyzing and understanding returns can provide valuable insights into the effectiveness of financial decisions and the potential for growth.

Return on Equity (ROE)

In personal finance, when you book a Fixed Deposit, you expect returns, which are measured as a percentage of the capital deployed. In India, it could range from 5-8%, depending on the economic circumstances. Similarly, companies also invest shareholders’ money into the business, which is called Equity Capital or Shareholders’ Capital, and this is expected to generate returns for the shareholders. This is called Return on Equity (ROE). If the company is generating a lesser ROE than the FD rates, then it simply means that even without running the business, had they just booked that money as an FD, they could have achieved better returns. On the other hand, the company is running a healthy business if the ROE is way beyond the prevailing FD rates.

ROE = Profit After Tax ( PAT) /Equity

(or) ROE = Earnings Per Share (EPS)/ Book Value Per Share (BVPS)

This metric is particularly vital for shareholders and investors as it indicates the company’s ability to reward them with significant returns on their investments.

Return on Capital Employed (ROCE)

If you find an opportunity where you can get a loan at 2% interest, and there is a bank that gives you 5% interest on a Fixed Deposit, wouldn’t you grab this opportunity? This is called Arbitrage, and there are companies who have mastered this and take debt to run the company, in addition to the equity funds from the shareholders. In such scenarios, apart from ROE, an important measure to check is whether the company is generating more money from the capital deployed to pay interest and still retaining some earnings or not. This measure is called Return on Capital Employed (ROCE).

ROCE = Earnings Before Interest and Tax (EBIT) / Capital Employed

(or) ROCE = Earnings Before Interest and Tax (EBIT) / Equity + Debt

ROCE is crucial because it assesses how efficiently a company uses all available capital to generate profits, including both its own and borrowed funds. It is an essential metric for business owners and management as it highlights the company’s operational efficiency and overall financial health.

Typical Values of ROE and ROCE

Typical values of ROE and ROCE can vary significantly across different industries.

Industries with high capital requirements, such as manufacturing or infrastructure, may generally have lower ROE figures due to significant investments in assets. On the other hand, industries that rely heavily on intangible assets, like technology companies, tend to have higher ROEs. A good ROE value varies depending on the company’s size, industry norms, and its growth stage.

As for ROCE, a figure higher than the company’s borrowing costs suggests efficient utilization of capital, while a value lower than the borrowing costs may indicate ineffective capital deployment.

Taking TCS India as Example.

PAT and EBIT can be found in the PnL Statement , Equity and Debt could be found in the Balance Sheet and below is a simple Example .

Financial Summary of TCS can be found here and we could consider for FY 22-23

Parameter

Value ( in Crores)

PAT

42303

EBIT

59259

Equity

366+90058 = 90424

Debt

7688

ROE = PAT / EQUITY

46%

ROCE = EBIT / Debt + Equity

60%

ROE of 46% and ROCE of 60% is really huge because they don’t have huge CAPEX and its in a service industry.

Summary

Both ROE and ROCE are essential financial metrics that provide valuable insights into a company’s performance and efficiency. ROE mainly focuses on the returns generated from shareholders’ investments, making it crucial for investors and shareholders. ROCE, on the other hand, takes a broader view by considering all capital employed, making it more relevant for business owners and management. While ROE is essential for assessing shareholder value, ROCE helps gauge the overall operational efficiency and profitability of a company. Ultimately, understanding both metrics and their implications can empower individuals and businesses to make informed financial decisions and drive sustainable growth.

Here’s the Comprehensive List of Our Blogs: Keep it Handy, Share with Friends and Family, Smash that Like Button, and Subscribe to Receive Blog Updates First. Your support fuels our passion for creating insightful content!

Disclaimer: This blog post is intended for informational purposes only and should not be considered as financial advice. Always conduct thorough research and consult with a qualified financial professional before making investment decision.