Life is a journey full of ups and downs, and Charlie Munger’s wisdom offers a simple guide to finding happiness. As someone from a middle-class Indian background, I have found his advice very helpful. Let me share how his ideas have shaped my life.

1. Avoiding Addictions

Addictions, whether to smoking, drinking, or bad habits, can ruin lives. I am grateful to my family and friends for helping me stay away from these traps. In a world full of temptations, having supportive people around you is crucial. Munger’s advice to avoid addictions reminds us to choose our influences wisely.

2. Letting Go of Envy

It’s easy to feel jealous when we see others doing well. But my friendships with people from different countries and my love for reading have taught me that nobody is perfect. Everyone has their own journey. By focusing on my own path, I have found joy in simply living. Munger’s wisdom helps us see that comparing ourselves to others only makes us unhappy.

3. Releasing Resentment

Traveling across India, I’ve seen both wealth and poverty. I’ve seen people living in luxury and others sleeping on the streets. These experiences have taught me to be grateful for what I have. Holding onto resentment only makes life harder. Munger’s advice encourages us to appreciate our own lives and let go of bitterness.

By sharing these thoughts, I hope to spread Munger’s simple yet powerful wisdom. His ideas have not only guided me but have also made my life richer. As we deal with life’s challenges, let’s remember that true happiness comes from being content, grateful, and wise enough to avoid envy, addiction, and resentment.

Summary : In his speech “How to Guarantee a Life of Misery,” Charlie Munger offers timeless advice on avoiding a life filled with unhappiness. He warns against falling into the traps of addiction, envy, and resentment. Inspired by Munger’s wisdom, I have embraced these principles in my own life as a middle-class Indian. By steering clear of addictions with the support of family and friends, letting go of envy through diverse friendships and reading, and releasing resentment by appreciating the varied experiences across India, I have found contentment and joy. Munger’s insights remind us that true happiness comes from being grateful and wise enough to avoid these common pitfalls.

Here’s the Comprehensive List of Our Blogs: Keep it Handy, Share with Friends and Family, Smash that Like Button, and Subscribe to Receive Blog Updates First. Your support fuels our passion for creating insightful content!

In today’s fast-paced world, financial literacy is more important than ever. Many of us were never taught about financial planning in school or by our parents, leaving us vulnerable to financial crises. If you’re one emergency away from bankruptcy, it’s time to take control of your finances. Here’s a straightforward guide to help you start your financial planning journey.

Step 1: Get Term Insurance

The first step in securing your family’s future is to get a term insurance policy. This is a cost-effective way to ensure that your loved ones are protected financially if something happens to you.

How Much Coverage Do You Need?

Use this formula to determine your total sum assured:

Total Sum Assured = ((Total Monthly Spend + EMI) / 50,000) * 1 Crore

This calculation ensures that your family can maintain their lifestyle even in your absence. Remember, you can discontinue this insurance once you have built a substantial financial cushion.

Step 2: Invest in Health Insurance

Medical emergencies can drain your savings faster than you think. A good health insurance policy protects you from unexpected medical expenses, allowing you to focus on growing your wealth.

Coverage Recommendations:

For Parents: At least ₹10 Lakhs per person.

For Yourself, Spouse, and Children: At least ₹5 Lakhs per person.

Don’t rely solely on employer-provided insurance. Create your own policy to avoid complications related to pre-existing conditions or waiting periods when switching jobs.

Step 3: Save Before You Spend

One of the simplest yet most effective financial habits is to save before you spend. Here’s how:

Open Two Bank Accounts:

Salary Account: Where your paycheck goes.

Savings Account: Transfer the necessary amount for EMIs and savings as soon as you receive your salary.

Spend What’s Left: Use the remaining balance in your salary account for your daily expenses. This method ensures that you prioritize savings and debt repayment.

Step 4: Plan for Retirement

A common rule of thumb is that for every ₹50,000 you need per month today, you will need ₹1 Crore at retirement. However, if you wish to maintain your current lifestyle, consider planning for ₹2 Crores for every ₹50,000.

Why the Increase?

As you age, your lifestyle may change, and inflation will affect your purchasing power. Observing your parents and in-laws can provide insight into the financial needs of retirement.

Step 5: The 15-15-15 Rule for Investing

Investing is crucial for building wealth. Here’s a simple rule to follow:

Invest ₹15,000 every month for 15 years.

Aim for a growth rate of 15% per annum.

By following this strategy, you could accumulate ₹1 Crore by the end of the investment period. Adjust your monthly investment based on your retirement goals and the number of Crores you need.

Where to Invest?

Achieving a 15% return is challenging but possible through well-researched mutual funds or direct equity investments. If you’re unsure, consider investing in index funds, which can provide a more conservative return of around 12%.

Conclusion

Financial planning may seem daunting, but taking these steps can help you secure your future and that of your family. Remember, I am not a certified financial planner or investment advisor; I am simply sharing lessons I’ve learned and practiced over time for educational purposes. Start your journey today, and take control of your financial destiny!

Here’s the Comprehensive List of Our Blogs: Keep it Handy, Share with Friends and Family, Smash that Like Button, and Subscribe to Receive Blog Updates First. Your support fuels our passion for creating insightful content!

In today’s busy India, where progress mixes with inequality, one pressing problem stands out: the growing gap between the rich and the poor. As the economy changes, this divide threatens to create more inequality in society. But in the midst of these challenges, we find solutions inspired by the ancient wisdom of Chanakya’s Arthashastra, showing us a path to a fairer and more balanced future.

The Rich-Poor Divergence

In recent years, the interplay between winners-take-all dynamics and crony capitalism has exacerbated the stark divide between the wealthy elite and the rest of society. This phenomenon, characterized by a small fraction of individuals amassing unprecedented wealth and power, often goes hand-in-hand with a system that fosters unfair advantages and privileges for the wealthy. As a result, we are witnessing an alarming concentration of wealth and influence among a select few, while many others struggle to make ends meet. This widening gap not only undermines economic fairness but also erodes social cohesion and mobility. Addressing this issue requires a comprehensive approach, including policies that challenge the entrenched advantages perpetuated by inherited wealth. One such policy area that warrants serious consideration is the reform of inheritance taxes, which play a crucial role in rebalancing economic opportunities and promoting a more equitable society.

Chanakya’s Taxation Tenets

Enter Chanakya, the ancient sage whose words continue to echo through the corridors of governance. In the Arthashastra, he delineates the principles of taxation with clarity and precision, advocating for its necessity in maintaining societal order and fostering economic prosperity. “Yatha shakti,” he proclaims, taxes should be levied according to one’s ability to pay, ensuring that the burden is borne equitably across society. Sanskrit Sloka: “Dharmo rakshati rakshitah” (Duty protects those who protect it) Chanakya’s dictum underscores the reciprocal relationship between the state and its citizens. By fulfilling their duties, citizens contribute to the stability and well-being of society, and in turn, the state must uphold its duty to safeguard their interests.

Inheritance Tax: A Pragmatic Solution.

In this light, inheritance tax emerges as a potent instrument for addressing the entrenched inequalities perpetuated through generational wealth accumulation. By levying taxes on inheritances above a certain threshold, we not only generate revenue for public welfare but also temper the tide of inherited privilege, leveling the playing field for all.

“Inheritance tax is not a punishment for success; it’s a catalyst for societal equity.”

By embracing this tax reform, we uphold the principles of Chanakya, ensuring that wealth is not concentrated in the hands of the few but circulates freely for the benefit of all.

Conclusion: Harmonizing Tradition with Progress

As we navigate the complexities of economic development and social cohesion, Chanakya’s wisdom serves as a guiding beacon, illuminating the path towards a more just and inclusive society.

In implementing inheritance tax, tailored to apply to inheritances above $1 million, we strike a harmonious balance between fiscal prudence and social equity, echoing the sage’s admonition against over taxation.

Sanskrit Sloka: “Sarve bhavantu sukhinah, sarve santu niramayah” (May all be happy, may all be free from illness) In this spirit of inclusivity and compassion, let us heed the lessons of the past to forge a brighter future for generations to come.

In summary, the proposition of inheritance tax in modern India not only aligns with the principles of fair taxation espoused by Chanakya but also represents a pragmatic response to the pressing challenge of wealth inequality. By embracing this approach, we can bridge the gap between the haves and the have-nots, creating a more harmonious and prosperous society for all.

Here’s the Comprehensive List of Our Blogs: Keep it Handy, Share with Friends and Family, Smash that Like Button, and Subscribe to Receive Blog Updates First. Your support fuels our passion for creating insightful content!

Disclaimer: This blog post is intended for informational purposes only and should not be considered as financial advice. Always conduct thorough research and con

In contrast to developed nations offering “Social Security” programs, India lacks a similar comprehensive support system for its citizens. The absence of such a safety net leaves individuals vulnerable to financial instability during retirement, sudden unemployment, disability, or loss of a spouse or parent. To address this gap, India introduced the National Pension Scheme (NPS) following the discontinuation of the old pension scheme. NPS aims to partially fulfill this role by encouraging individuals to save regularly, with contributions invested in a mix of equities, corporate bonds, and government bonds to generate returns that can safeguard their retirement years.

To be eligible for the National Pension System (NPS), you must:

Be an Indian citizen, either a resident, non-resident, or Overseas Citizen of India (OCI).

Be between 18 and 70 years old as of the application date.

Comply with the Know Your Customer (KYC) norms in the application form.

Be legally able to sign a contract under the Indian Contract Act.

Not already have an NPS account.

Work in a corporate that has adopted the NPS scheme.

What is the Minimum Amount one should invest in NPS & is there any Maximum Limit ?

The minimum initial contribution to the National Pension Scheme (NPS) is Rs 500. You must make these contributions when you register, and you must contribute at least once a year, with a minimum contribution of Rs 1,000. There is no Maximum limit on the NPS maximum contribution per year, any investment above 2Lakhs threshold will not be eligible for tax deductions.

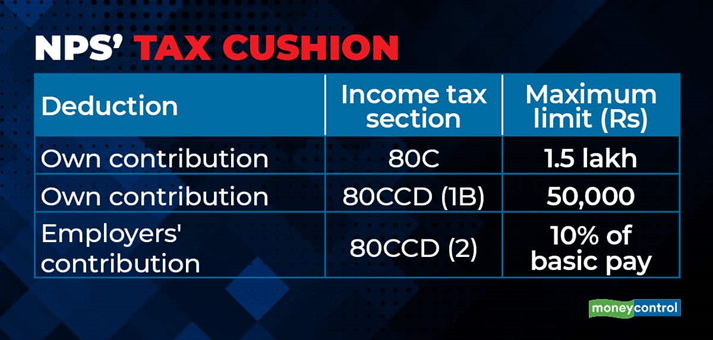

A tax exemption of Rs. 1.5 lakh can be claimed on the employee’s and employer’s contribution towards the National Pension System (NPS). Tax benefits can be claimed under Section 80CCD(1), 80CCD(2), and 80CCD(1B) of the Income Tax Act.

Where will my money be invested & how is the historic returns looking like ?

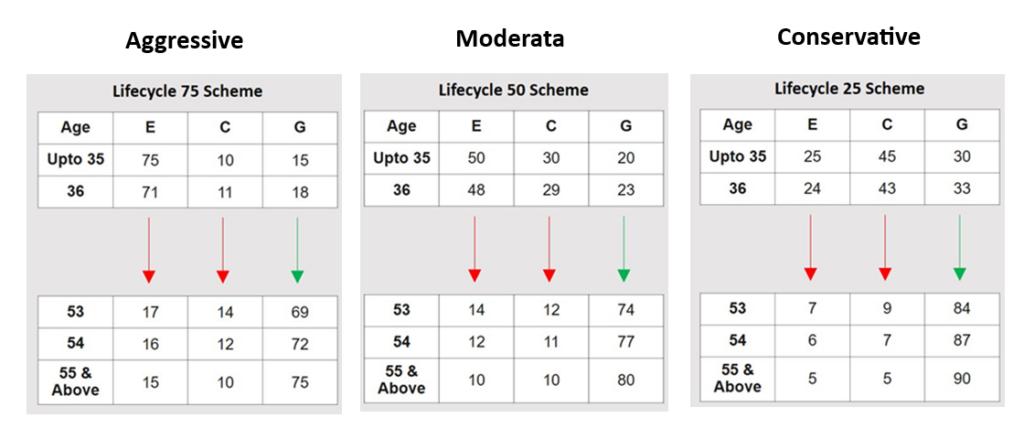

In NPS, you have the option to choose how your money is invested in different asset classes. These are known as ECG in NPS – Equity (E), Corporate Debt (C), Government Securities (G), and Alternative Investment Funds (A).

Equity can be thought of as buying stocks, Corporate Debt as similar to fixed deposits in private banks, and Government Securities as akin to purchasing Kisan Vikas Patra or National Saving Certificates from the Post Office. While Equity involves higher risk with potentially higher returns, Government Securities carry lower risks and offer modest returns that may just surpass inflation.

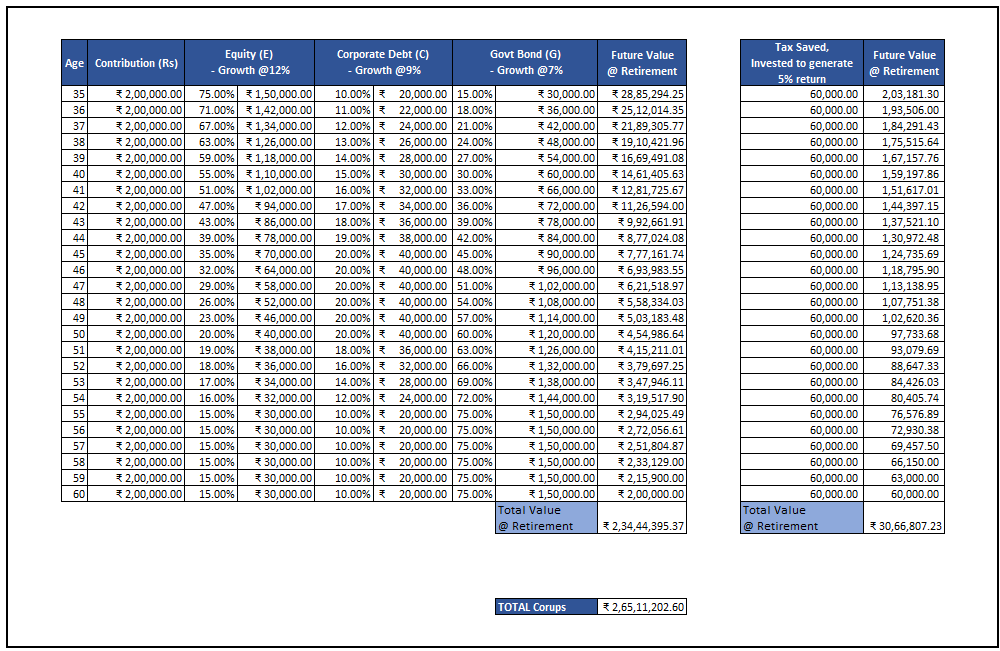

Even for those inclined towards risk-taking, there are restrictions on the extent of Equity exposure permitted. The most aggressive choice allows for a maximum Equity exposure of 75% at the age of 35, gradually decreasing to 15% beyond 55 years of age.

How are the returns looking like in Equity for NPS ?

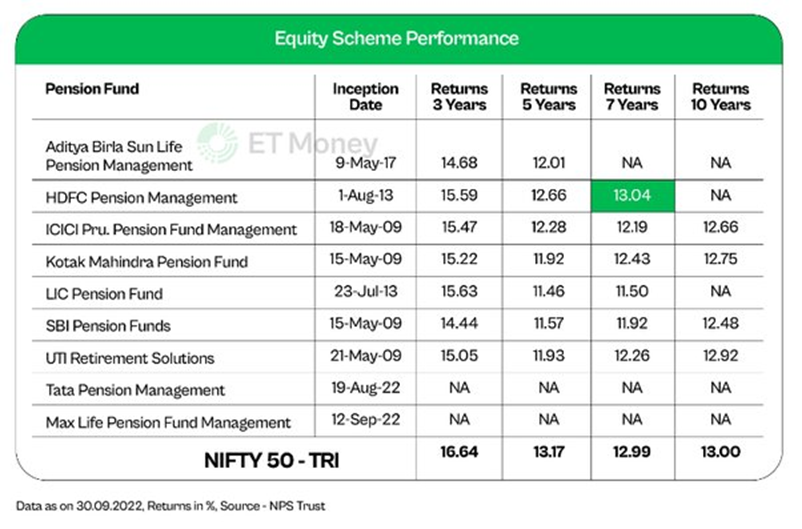

Although one gets an exposure to Equity , the catch is one cannot go pick the stock , it has to be done by a Pension Fund which one has opted for , they could invest in Index stocks or the Index funds itself. Data published by NPS Trust reveals that on a long term horizon Equity schemes have provided returns around 12% at max.

When One check the Index Funds return for 10+ years it looks almost similar or slightly superior, it comes to around 13% returns.

1% might look small but when compounded would make a significant difference over a long period of time, this must be dealt in great detail.

What if I opt for Index Mutual Fund instead of NPS ?

Lets do the math to understand how NPS and Index Mutual Fund behave in the long horizon , let us also consider the most hyped tax savings component in NPS as well to get a fairer picture.

Some assumptions i am going with are , One is investing a maximum of Rs. 2.0 Lakhs per year beyond which there is no tax benefits , One choose Aggressive Choice else the returns would be even more mediocre. The Tax saved is booked in as FD which would generate 7% per year and the taxes on interest is deducted leaving us with an yield of 5% per annum.

So one would be left with a corpus of Rs. 2.65 Cr at the time of retirement.

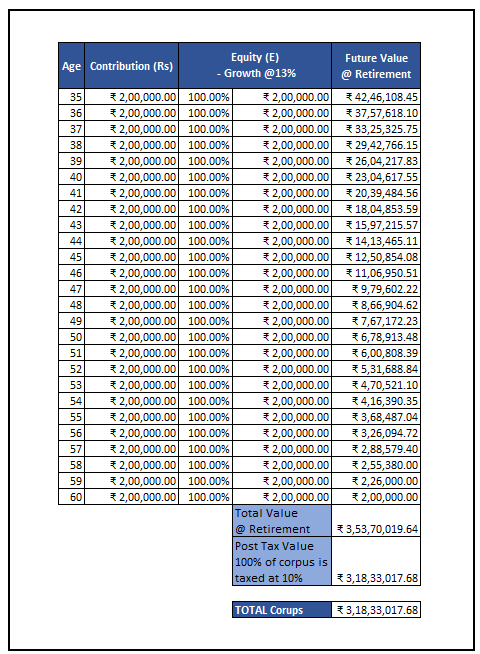

Now let us see what happens to the same money when invested in NIFTY50 Index Mutual Fund .

One would be left with a corpus of Rs.3.18 Cr at the time of retirement.

Conclusion :

In my assessment, even a basic calculation indicates that the returns from NPS are mediocre. Moreover, when compared to index funds, the risk of losing my retirement savings is evident, leading me to conclude that it’s definitely not the right choice for me.

Here’s the Comprehensive List of Our Blogs: Keep it Handy, Share with Friends and Family, Smash that Like Button, and Subscribe to Receive Blog Updates First. Your support fuels our passion for creating insightful content!

Disclaimer: This blog post is intended for informational purposes only and should not be considered as financial advice. Always conduct thorough research and consult with a qualified financial professional before making investment decision.

Unveiling the Art of Stock Investing: Expertise, Dedication, and the Gift of Time

Delving into the world of stock investing requires a blend of expertise, dedication, and a generous investment of time. Firstly, becoming adept at analyzing businesses is akin to becoming a detective. It involves scrutinizing a company’s financial statements – the balance sheet, income statement, and cash flow statement – to understand its health. This financial sleuthing also extends to assessing a company’s growth potential, competitive positioning, and the broader sector trends in which it operates. This expertise doesn’t happen overnight; it’s a continuous learning process.

Dedication is the backbone of successful investing. Monitoring the stock market demands a commitment to staying informed about global and industry-specific news, economic changes, and shifts in market sentiment. Understanding the intricacies of financial markets and developing a keen sense for when to act or hold requires persistent effort.

Time is the unsung hero of the investing journey. Just as Rome wasn’t built in a day, a well-constructed stock portfolio takes time to evolve. Patience is crucial, as markets can be unpredictable in the short term. Regularly reviewing and adjusting your investment strategy, and being prepared for the long haul, is part of the time investment required.

In essence, becoming a savvy stock investor is not just about buying and selling; it’s about honing analytical skills, staying dedicated to the market’s pulse, and giving investments the time they need to flourish. This trio of expertise, dedication, and time is the winning combination for those navigating the exciting yet complex world of stock investing.

Simplicity in Diversity: The Effortless Journey of Investing in Mutual Funds

Investing in mutual funds offers a straightforward and user-friendly path for those seeking a hands-off approach to building wealth. The process begins with selecting a mutual fund that aligns with your financial goals, time horizon, and risk tolerance. Unlike scrutinizing individual stocks, this involves evaluating the fund’s historical performance, expense ratio, and the expertise of the fund manager. Effort is considerably reduced as you’re essentially placing your trust in the hands of experienced professionals who manage the fund’s portfolio.

Once the choice is made, purchasing mutual fund shares is a breeze, often just a few clicks away through an online platform or with the assistance of a financial advisor. The beauty of mutual funds lies in their inherent diversification – your investment is spread across a variety of assets, reducing the impact of a poor-performing individual investment.

Tracking a mutual fund is simpler compared to managing a portfolio of individual stocks. Regular updates on the fund’s performance are readily available, allowing investors to gauge how well it aligns with their objectives. The fund manager takes on the responsibility of adjusting the portfolio to maximize returns within the fund’s defined strategy.

Selling mutual fund shares is also uncomplicated. Investors can redeem their shares at the current net asset value (NAV), providing liquidity and flexibility. The exit decision is often tied to changes in your financial goals, time horizon, or risk tolerance.

The icing on the cake is having an experienced fund manager at the helm, making tactical decisions on behalf of investors. Despite the expertise involved, mutual funds typically charge a modest management fee, allowing investors to benefit from professional management while keeping costs reasonable. In essence, investing in mutual funds offers a hassle-free experience, combining the simplicity of the process with the expertise of a seasoned fund manager to navigate the financial markets on your behalf.

You can read more about Mutual Funds here and then here

Why I choose Direct Stock Investing over Mutual Funds and why I don’t blindly recommend my approach for all ?

Certainly! Here’s a refined version of your idea with improved grammar, sentence formation, and spelling:

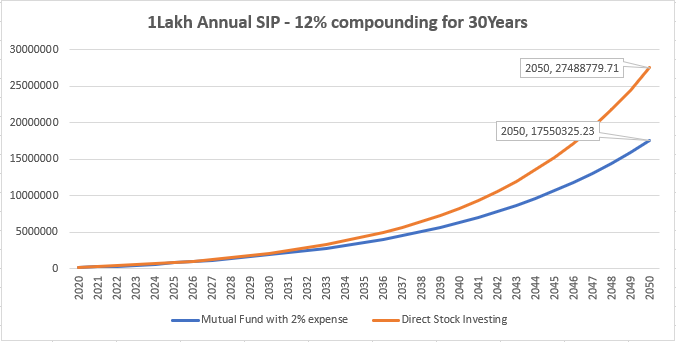

Upon analyzing the financial landscape, a compelling argument surfaces in the realm of investment strategies. Consider a scenario where one invests directly in stocks, allocating 1 lakh per year for 30 years, with an assumed annual growth rate of 12%. The outcome is a substantial 2.7 Crores at the end of the period. Contrastingly, envision investing in a mutual fund, maneuvering through various funds while maintaining the same growth rate of 12%. However, factor in the 2% annual toll for entry criteria, expense ratio, and exit load to the mutual fund house. The result? A take-home amount of 1.7 Crores, marking a staggering loss of over 1 Crore, translating to nearly a 30% deficit.

While one might argue that transaction frequency might be lower or the charges could be less than the stipulated 2%, the counterargument asserts that diligent analysis can potentially yield more substantial returns in direct stock investing. The crux of the debate lies in the significance of a 30% surplus post 30 years versus the present commitment of time and effort required for understanding, investing, and tracking.

For individuals like me who are coming from a lower-middle-class background, the prospect of 30% additional funds after three decades holds paramount importance. It not only secures financial stability but also offers a competitive advantage. The time spent from in-depth financial analysis can be redirected towards self-improvement in diverse areas such as economics, geopolitics, resource optimization, and leadership skills. This multifaceted skill set can contribute to career growth, potentially leading to increased income. With the newfound financial flexibility, one could even enhance their SIP contributions over the years, generating substantial returns upon retirement.

However, it’s crucial to acknowledge that this perspective may not resonate universally. Individuals who prioritize present-day time constraints, value simplicity, and are uninterested in delving into the complexities of business analysis may find comfort in the ease of mutual fund investments. The choice between direct stock investments and mutual funds ultimately hinges on personal preferences, financial goals, and the perceived trade-off between immediate convenience and long-term financial gains.

Here’s the Comprehensive List of Our Blogs: Keep it Handy, Share with Friends and Family, Smash that Like Button, and Subscribe to Receive Blog Updates First. Your support fuels our passion for creating insightful content!

Disclaimer: This blog post is intended for informational purposes only and should not be considered as financial advice. Always conduct thorough research and consult with a qualified financial professional before making investment decision.

Introduction: Lost in the Race, Forgotten ‘Enough’.

In the relentless pursuit of wealth, we find ourselves caught in the rat race, often forgetting to pause and ask a fundamental question: how much is truly enough? Reflecting on my own journey, I recall that as a child, I believed having 10 lakhs would make life heavenly. However, with time, my aspirations escalated; from dreaming of 1 crore, I eventually aimed for 100 crores, influenced by societal notions of luxury. Reading “The Psychology of Money” by Morgan Housel unveiled a universal truth – this desire for more is an endless cycle. Even the wealthy yearn for greater wealth: Michael Jordan eyes Jeff Bezos, and Bezos eyes Elon Musk.

In a moment of contemplation, a lingering question emerged within me: “What is the threshold of sufficiency?” Turning to the wisdom of my guru, Acharya Chanakya, I discovered his profound insight: “

the moist important thing for a happy life is satisfaction. If you are satisfied with life then there will be no problem in your life.”To be satisfied , one must know how to control his senses. No one is happier than the person who is satisfied by controlling his senses.”

Thus began my quest to explore the concept of “enough.”

The Cost of Chasing More: Tragedies Unveiled.

Conversations with my friends opened my eyes to some harsh realities. One friend had spent ten years building up money, but lost it all in just a few months by trading in ways that were very risky. He was convinced by his colleagues that he could make more money quickly by trading instead of saving for a small piece of land.

Another friend shared that their family ran a chit fund, but things went wrong and they lost all the money they were taking care of for others. This led them to bankruptcy.

While growing up, I saw many people from lower middle-class families lose everything because they hoped to get rich quickly. They gambled all their money, even the little they had, just to avoid the shame of being broke.

My own family also struggled with money. We had times when we had to walk a long way to save a small amount of money, just to buy a simple snack.

Seeing all of these situations shaped how I handle money. It made me wonder: Is it really worth it to chase after money so much that we lose out on life, time for ourselves, and our self-respect?.

Purpose and Passion: The Dual Pathways of Life.

As we progress through life, our selection of business or profession naturally transforms. For certain individuals, their work becomes a channel through which they find a profound sense of purpose and fulfillment. However, contrasting this, there are those who find themselves trapped in roles that bring about dissatisfaction and resentment.

Irrespective of the specific circumstances, the notion of constructing a financial corpus gains paramount importance. This corpus serves as a reservoir of financial resources, a reservoir that is integral to attaining a state of financial independence. This state liberates individuals from the compulsion to work solely for monetary gain, thereby affording them the luxury to delve into their passions and interests with unbridled enthusiasm.

In essence, the strategic accumulation of wealth doesn’t solely cater to material acquisitions, but rather, it acts as a conduit to a more profound form of freedom. This freedom extends beyond merely quitting a disliked job; it empowers one to explore their innate potential, nurture their creative endeavors, and lead a life aligned with their true aspirations.

Unleashing the Potential: The Miraculous 2 Crore Corpus.

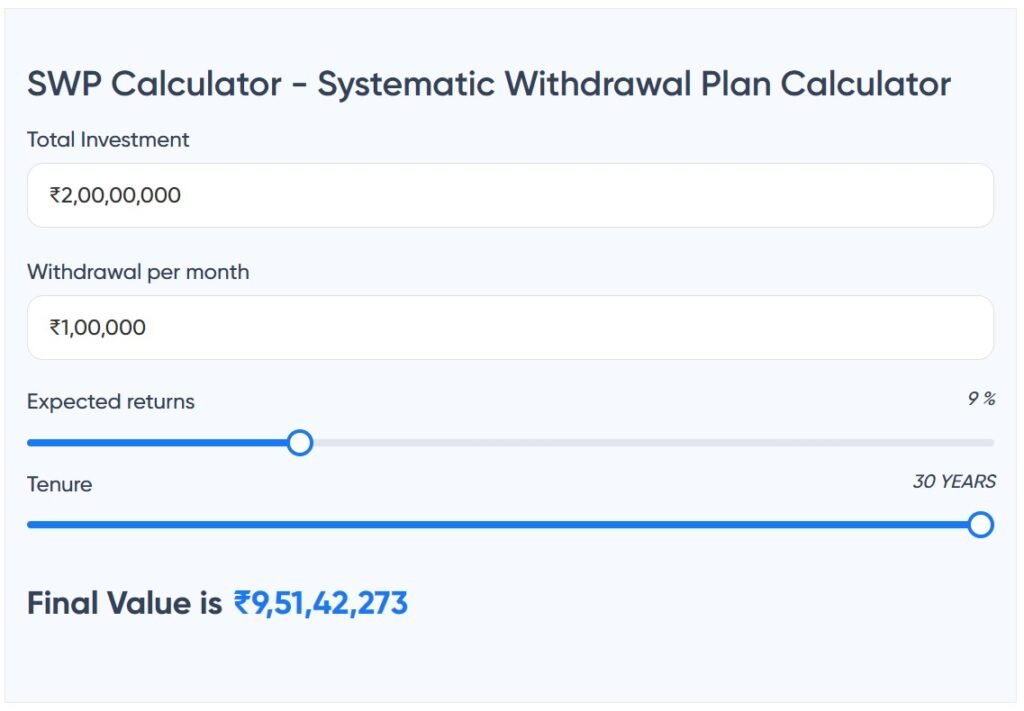

Let’s consider a scenario where an individual, through ethical means, manages to accumulate 2 crores in their business or profession. Imagine this sum being invested in an Indian index fund, which hypothetically yields a 9% year-on-year return (being conservative here, considering that historically NIFTY has averaged 12%). Suppose this person withdraws 1 lakh every month for 30 years, allowing the remainder to continue compounding. Surprisingly, at the end of these 30 years, the corpus would still amount to a substantial 10 crores!

This prompts us to question: do we truly require such a substantial amount of money? With age, our need for extravagant luxury often diminishes. By having comprehensive health insurance in place, monthly expenses could be significantly reduced.

After conducting this thought experiment, I found myself taken aback and pushed to delve deeper. Could I realistically aim to amass 2 crores and attain a form of financial independence? Certainly, this wouldn’t imply ceasing work, but rather, it would infuse a heightened sense of confidence and contentment into life. Wouldn’t that be a valuable achievement?

I’m not certain if 2 crores is “The” figure that applies to me. What I wish to emphasize to the reader is that each individual should take a pen and paper to ascertain this number. Without doing so, breaking free from the rat race can seem nearly impossible.

Upon reaching the juncture where our accumulated corpus is capable of consistently generating the desired monthly revenue while also undergoing substantial compounding, a pivotal decision arises. This crossroads invites us to consider bidding farewell to the professions that evoke our disdain or the jobs that no longer kindle our interest. The financial security provided by the self-sustaining corpus can empower us to relinquish roles that once held us captive in the pursuit of monetary gains, paving the way for new chapters aligned with our genuine passions and aspirations. This transition signifies a transformative shift from obligation to choice, from the compulsion of necessity to the liberation of fulfillment.

Dharma’s Light: Transforming Desires into Destiny.

Here come the natural question how do i find my passion?

Well its not that easy to answer , but not difficult either …

I can only quote some awakening links from the Sanathana Dharma.

Dharma is your unique purpose in life. It is the process by which you use your unique skills and passions to serve your community and the world.

There is a phrase in the Upanishads, one of the great Indian texts, that says:

” You are what your deepest desire is,

As is your desire, so is your intent,

As is your intent, so is your will,

As is your will, so is your deed,

As is your deed, so is your destiny. “

Wisdom from Mahabharata: Navigating the Battle Within for a Noble Life.

As we embark on the quest to discover a meaningful purpose for our lives, it’s crucial to bear in mind the insightful encapsulation of the Mahabharata by a wise individual:

“Mahabharata in a metaphorical way: the battle of Mahabharata is, actually, the battle between the good and evil present in ourselves; this means that we are composed out of forces of evil and of good. Our mental condition is not void: forces of evil and of good are present in us. Therefore, we cannot wait and see: we ought to take a decision on our moral constitution.”

Here’s the Comprehensive List of Our Blogs: Keep it Handy, Share with Friends and Family, Smash that Like Button, and Subscribe to Receive Blog Updates First. Your support fuels our passion for creating insightful content!

Disclaimer: This blog post is intended for informational purposes only and should not be considered as financial advice. Always conduct thorough research and consult with a qualified financial professional before making investment dec

Understanding Stock Movements: Long-Term Business Growth vs. Short-Term Speculation.

When it comes to stock movements, investors often witness two main driving forces: long-term business growth and short-term speculation. Business growth refers to the underlying performance of a company, including revenue growth, profitability, market share, and expansion plans. These factors influence the stock’s value over the long run and attract investors seeking sustainable returns.

On the other hand, short-term speculation is driven by market sentiments, news, rumors, or macroeconomic factors that cause rapid price fluctuations. Speculative investors aim to capitalize on short-lived price movements and often trade frequently based on these transient factors.

Understanding the distinction between these two forces is crucial for successful investing. Long-term investors focus on the fundamentals of the business, studying its competitive advantage, management team, industry trends, and growth potential. They ride the ups and downs, confident that the company’s strong fundamentals will drive the stock price over time.

Weathering the Storm: The Initial 5-10% Stock Dip.

One of the most nerve-wracking experiences for investors is witnessing their newly invested stock take a nosedive shortly after buying it. It’s essential to remember that the stock market is highly volatile and influenced by a myriad of factors, including investor emotions and speculative activities. A short-term dip in stock price doesn’t necessarily reflect the true value of the company or its long-term prospects.

To navigate these turbulent waters, investors must resist making impulsive decisions driven by fear and instead remain focused on their investment thesis. They should evaluate the reasons for the dip, discerning whether it’s related to business fundamentals or merely market sentiment. Often, such temporary declines present an excellent opportunity to accumulate more shares at a discounted price, amplifying future gains when the stock eventually rebounds.

The Long Horizon: The Importance of Conviction in Investing.

Investing with conviction means having complete faith in the companies you invest in and their long-term growth potential. Conviction-driven investors don’t panic during short-term market fluctuations because they have extensively researched the company’s financial health, competitive landscape, and management credibility.

When investors adopt a long-term perspective, they align their goals with the company’s growth trajectory, understanding that businesses experience ups and downs over time. Warren Buffet, one of the most successful investors, famously said, “Our favorite holding period is forever.” This approach emphasizes the value of patience, allowing the compounding effect to work its magic over extended periods.

Unveiling the Magic of Compounding Effect: A Tale of Two Investments with a small difference of returns per year.

A small investment of 15,000 INR per month consistently for 15 years in an asset that is generating 15% per annum would make one a “CROREPATI.” The key lies in selecting the right asset and staying the course consistently. Despite the investment being only around 27lakhs, the power of compounding and the choice of a high-yielding asset can lead to extraordinary wealth.

The only difference between Investment 1 and Investment 2 is the asset yield. In Investment 1, it was 15%, while in Investment 2, it was 14%. At first glance, this might seem like a small difference, but over the course of 10 years, it has made a significant impact, resulting in a difference of around 10lakhs in the final cumulative value. This underscores the remarkable effect even a slight variation in returns can have on long-term investments.

Embracing the Einstein Effect: The Power of Compound Interest.

Albert Einstein famously said, “Compound interest is the eighth wonder of the world. He who understands it, earns it … he who doesn’t … pays it.” This statement not only applies to financial investments but resonates in various aspects of life.

In conclusion, the path to financial success lies in embracing the power of patience and compounding in investing. By understanding the true drivers of stock movements, maintaining conviction in solid investments, and harnessing the magic of compounding, investors can unlock the full potential of their wealth. Remember, fortune favors the patient and disciplined, and the wonders of compounding can transform your financial journey into an extraordinary one.

Here’s the Comprehensive List of Our Blogs: Keep it Handy, Share with Friends and Family, Smash that Like Button, and Subscribe to Receive Blog Updates First. Your support fuels our passion for creating insightful content!

Disclaimer: This blog post is intended for informational purposes only and should not be considered as financial advice. Always conduct thorough research and consult with a qualified financial professional before making investment decision.

In this blog, I share my journey of rational investment and how I consistently selected the right investment vehicles to achieve my financial goals. Starting at the age of 12, I learned the value of saving and progressed from fixed deposits to purchasing items like a cycle and computer. Later, I began planning for retirement after the birth of my child. Although I don’t invest in mutual funds personally, I recognize their potential and explain how I approach savings and the considerations to choose the right mutual fund vehicle for specific goals.

Remember, each person’s financial circumstances and goals are unique. Therefore, it’s crucial to conduct thorough research and seek tailored professional guidance. Before diving into investment strategies, ensure you have adequate health insurance and term insurances to safeguard your financial stability. Join me on this enlightening exploration of rational investment as we delve into choosing the right investment vehicle and the thought process behind it.

To effectively achieve my financial goals, I prefer categorizing them into short term, medium term, and long term. This classification allows me to adopt different approaches for each category, ensuring a balanced and strategic investment plan. By clustering my goals in this manner, I can focus on specific timeframes and tailor my investment strategies accordingly. In the following sections, we will explore each category in detail and examine the approaches I employ to achieve success in each. From short term objectives that require liquidity and quick returns, to medium term goals that involve moderate risk and growth potential, and finally, long term aspirations that prioritize wealth accumulation and retirement planning, this holistic approach enables me to optimize my investments and realize my financial ambitions.

I recommend reading this blog before you continuing if not done already – Link

Securing Short-Term Goals: The Power of Debt Mutual Funds and Fixed Deposits.

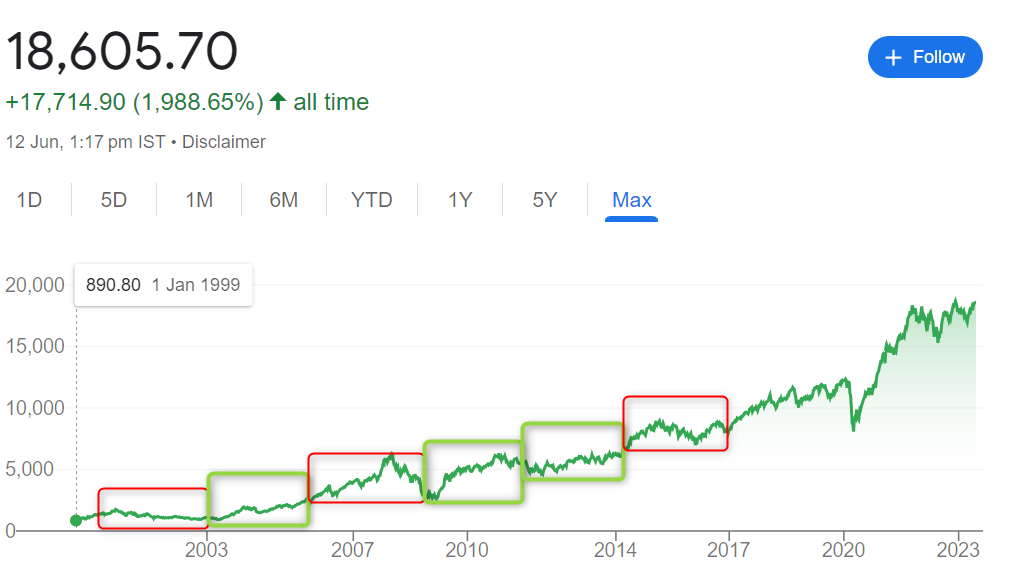

Let’s consider the example of NIFTY50 to evaluate whether the stock market or equity investments are suitable for short-term investments. Upon examining the chart below, we can observe that there are significant inconsistencies in the returns over different two-year periods. Some two-year blocks have yielded positive returns, while others have resulted in negative returns.

By analyzing the historical performance of NIFTY50, it becomes evident that the stock market can be volatile and unpredictable over short timeframes. The fluctuating nature of stock prices makes it challenging to accurately predict short-term outcomes. While there have been periods of positive returns, there have also been instances where investments in the stock market have led to losses within a two-year period.

When it comes to short-term goals with a specific timeframe of 2-3 years, such as buying a MacBook, purchasing a DSLR camera, or going on a Euro trip, the financial objective is clear and the required amount of money is known. In this case, buying stocks / mutual funds that have exposure to stocks ( equity) may not be the most suitable option due to the uncertainty of returns within such a short timeframe. Instead, two viable options for achieving these short-term goals are investing in a debt-focused mutual fund or opting for Fixed Deposits.

Debt-focused mutual funds provide an attractive alternative, offering full exposure to debt instruments while minimizing or completely avoiding exposure to equity. These funds invest in fixed-income securities like government bonds and corporate bonds, which provide a regular stream of income and potentially stable returns. By selecting a mutual fund that aligns with your risk tolerance and investment horizon, you can effectively accumulate the necessary funds for your short-term goals.

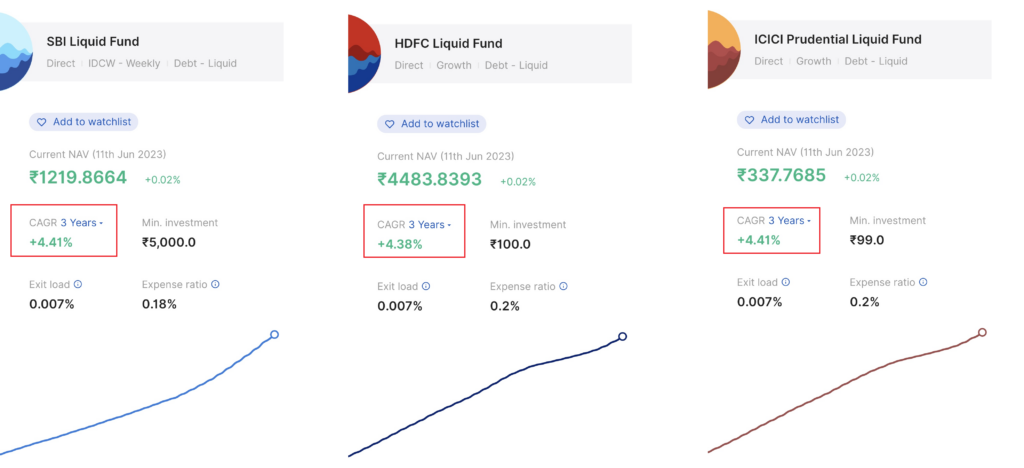

Typical Mutual Funds in the short run have roughly given 4-4.5% returns in the past 3 years as on today and the chances of this repeating for the next 3 years is higher !

Fixed Deposits is another option for short term investing , which provide a secure and predictable way to grow your savings. By depositing a specific amount for a predetermined period, you earn a fixed interest rate. Fixed Deposits offer stability and ensure that your money will be available when you need it to fulfill your short-term aspirations.

Typical Fixed deposits as on today are offering 7.0-7.5% returns over the next 3 years and seems more attractive over debt funds .

“Currently”, I find Fixed Deposits more appealing than debt mutual funds for my short-term needs. However, it is important to recognize that circumstances can change over time. When making investment decisions, I will assess the prevailing situation and adapt my strategy accordingly. By continuously evaluating and adjusting my approach, I can ensure that my investments align with the evolving market conditions and my specific financial goals. Flexibility and adaptability are key when navigating the dynamic nature of the investment landscape.

Balancing Risk and Reward: The Case for Equity Mutual Funds in Achieving 5-7 Year Goals.

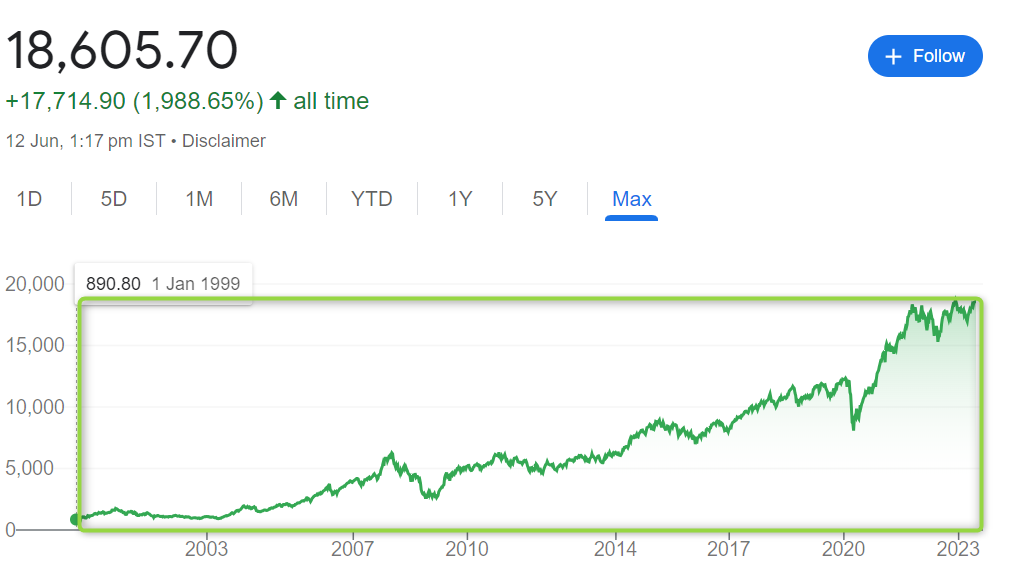

Let’s consider the example of NIFTY50 again to evaluate whether the stock market or equity investments are suitable for medium-term investments. Upon examining the chart below, we can observe that there are significant consistencies in the returns over different seven-year periods. all of them have got positive returns, may be at different rates but are in general positive .

It is more or less clear that equity is a great option for mid term investing but the problem doesn’t end here , this is just opening up a new bunch of problems

There are wide range of Mutual funds that are exposed to equity are available in the market today ,The options range from index funds to small-cap, large-cap, mid-cap, and hybrid funds.

While I understand the confusions that arise, based on my rationale, I would prefer to refer to the following table for guidance.

Flexibility of Goal

Recommended Product

Rational

Not Flexible

Hybrid Funds

Risk is lesser, so are the rewards due to exposure to debt instruments

Slightly Flexible

Aggressive Hybrid Funds

Slightly higher risk, with slightly lower returns due to the presence of debt

Flexible

Index Funds / Equity Funds

Slightly higher risk, but higher returns as they have 100% exposure to equity

Extremely Flexible

Mid Cap / Small Cap Funds

High risk and potentially high rewards due to exposure to mid/small-cap stocks

Building Wealth for Retirement: Why Equity is Key to Long-Term Savings.

Let’s consider the example of NIFTY50 again to evaluate whether the stock market or equity investments are suitable for long-term investments. Upon examining the chart below, we can observe that in the long run stock market / equity gives real good returns , it is in-fact the same in any developing countries.

A recommended strategy for long-term savings is to begin investing in a combination of small-cap and index funds early in one’s career. Allocating funds equally between these two categories allows for growth potential and broad market exposure. As individuals approach retirement, gradually shifting the allocation towards index funds provides stability. Upon retirement, it is advisable to consider moving the portfolio into risk-free options like fixed deposits or debt funds to preserve capital. This strategy should be personalized based on individual circumstances and regularly reviewed with a financial advisor.

Selecting the Right Mutual Fund: Unveiling the Rational Behind Fund House and Manager Evaluation.

When it comes to choosing the right mutual fund, considering the track record of the fund house and the expertise of the fund manager becomes crucial. Investors should conduct thorough research on the fund house’s reputation, stability, and financial performance. Exploring online resources ( googling ) and financial news platforms can provide valuable insights into the fund house’s history, any reported fraud cases, and overall credibility.

Additionally, evaluating the specific mutual funds offered by the fund house requires assessing factors such as entry costs, exit loads, and expense ratios. Comparing these costs among different funds can help investors make an informed decision that aligns with their financial goals and risk tolerance. It’s important to note that investment decisions should not solely rely on past performance but should be combined with an understanding of the fund’s investment strategy and objectives.

Once invested, staying vigilant is essential. Investors should regularly check for any newsletters or updates shared by the fund house, as these communications often provide insights into market trends, fund performance, and any changes in the investment strategy. Additionally, keeping an eye on financial news and reports about any fraud or controversy related to the fund house can help investors stay informed and take necessary actions if required.

Conclusion :

In conclusion, comprehending the suitability of investment vehicles for short, medium, and long-term goals is crucial. For short-term objectives, fixed deposits and debt mutual funds offer stability. Medium-term goals benefit from a combination of small-cap and index funds. For long-term aspirations like retirement, equity investments provide growth potential. Thorough research on fund houses and managers, evaluating past performance, costs, and staying informed through newsletters and news sources are essential practices. Seek professional advice and adapt strategies as needed. Empower yourself with knowledge and diligence to navigate the complex world of investments and work towards financial success.

This is a good Place to start ones mutual fund’s journey I believe : Coin by Zerodha.

Want to learn why I choose direct equity investment over mutual funds? – A new post discussing this topic will be published soon, please follow my blog page.

Here’s the Comprehensive List of Our Blogs: Keep it Handy, Share with Friends and Family, Smash that Like Button, and Subscribe to Receive Blog Updates First. Your support fuels our passion for creating insightful content!

Disclaimer: This blog post is intended for informational purposes only and should not be considered as financial advice. Always conduct thorough research and consult with a qualified financial professional before making investment decision.

Dividends, the distributions of a portion of a company’s earnings to its shareholders, play a crucial role in the financial landscape. In this section, we will explore the concept of dividends and delve into the reasons why companies choose to pay them out. Understanding dividends is essential for investors seeking stable income streams and long-term wealth accumulation.

Why do companies choose to pay Dividend to Investors ?

Dividends represent a portion of a company’s profits that is shared with its shareholders. By paying dividends, companies reward their shareholders for their investment and participation in the company’s growth. This practice is not only a means of showing appreciation but also a strategic move to attract investors by offering an incentive beyond capital appreciation. Dividends can be a sign of a healthy and well-established company, instilling confidence in investors and attracting long-term shareholders.

In the above example, it can be observed that the company has consistently earned money year over year (YOY) and distributed dividends to investors, amounting to over 30-40% of its annual earnings. The remaining earnings are retained in the company’s balance sheet for reinvestment and further growth.

Consistent dividend payments distinguish good companies, while the mark of great companies lies in their consistent dividend increases over time. By maintaining a reliable dividend payout, good companies demonstrate their commitment to rewarding shareholders. On the other hand, great companies exhibit their exceptional financial strength and growth potential by consistently raising dividends, showcasing their ability to generate sustainable profits and create long-term value for investors

Why should one consider dividend yielding stocks in their portfolio?

If you had purchased TCS shares at Rs.140/- in the middle of 2005 and held onto them until now, not only would the stock have risen to Rs.3500/-, but you would by now also have started receiving approximately Rs.50/- per year as dividends.

Power of Dividend for long term investors.

Dividend Compounding : Investing in the right company and holding onto the shares for an extended period can yield remarkable results. Imagine purchasing shares of a company today at Rs.100 /- and remaining invested as the company grows and prospers over the decades. In such a scenario, it is entirely possible that after a few decades, you could receive an annual dividend of Rs.100 /- for each share you own, in addition to the substantial appreciation in the share price that occurred over the years.

During the stock market crash caused by COVID, had you purchased Karnataka bank stocks at Rs.35/-, you would now be receiving Rs.4/- or more as dividends every year, according to their dividend policy. This would represent a return of over 10% annually, excluding any potential stock price appreciation.

Buying Dividend yielding stocks at the right time.

Steal Deals: Dividends are not solely a long-term game; they also provide short-term opportunities for investors to achieve attractive yields. By making astute stock purchases at opportune moments, it is possible to generate returns that surpass traditional fixed deposit rates within a few years. With dividends often increasing over time as companies expand, investing in dividend-paying stocks presents the potential for substantial returns that go beyond long-term strategies. This dynamic nature of dividends allows investors to benefit from both short-term income and long-term growth, making them a compelling option for maximizing investment gains.

What factors do I considered when determining the appropriate allocation of dividend yielding stocks in my portfolio?

Dividend income can play a crucial role in retirement planning ( This need not be at 60 but when planned well can happen much earlier ). As individuals approach retirement from their 9 to 5 job , they often seek stable and reliable sources of income to support their lifestyle. Dividends can provide a steady stream of passive income, as many companies distribute a portion of their earnings to shareholders on a regular basis. This dividend income can serve as a valuable addition to other retirement income sources.

By investing in dividend-paying stocks or funds, retirees can potentially enjoy a consistent cash flow that helps cover living expenses and maintain financial security throughout their retirement years. Additionally, dividend income can offer a hedge against inflation, as many companies increase their dividend payouts over time, helping retirees preserve the purchasing power of their income. Overall, incorporating dividend income into retirement planning can provide retirees with a reliable and potentially growing source of funds to support their post-career lifestyle.

Some of the key elements I consider before adding dividend stocks to my portfolio.

While my main focus is on growth stocks, I’m open to attractive dividend yields in the market, such as the Karnataka bank example mentioned earlier. A balanced approach, combining both growth and dividend-yielding stocks, can optimize portfolio returns.

I believe that dividend-yielding stocks are more suitable for retirement planning, and I do not think it is advisable to add a significant number of dividend stocks to my portfolio early in my career. Doing so could potentially limit the growth potential of my capital.

Even during retirement, I don’t believe in allocating all my funds to dividend-yielding stocks. I understand that the decision to distribute dividends lies solely with the board of the company, and as a shareholder, I have no direct control over it. Dividend-yielding stocks form only a partial portion of my portfolio. For the remaining portion, I prefer investing in corporate bonds and fixed deposits.

What strategies or methods I employ to identify dividend yielding stocks?

Whether I’m investing for stock price appreciation or dividends, the fundamental checks I perform remain largely unchanged. However, when it comes to dividend-yielding stocks, there are certain liberties and considerations I take into account.

Will the products that the company is selling today still be in demand after a decade?

Does the company have a policy that mandates the payment of dividends during the normal course of business?

Has the company consistently paid out dividends in the past?

Are the company’s financials healthy – company shall pay dividend from its free cash flow and not via debt or equity dilution?

Are the promoters clean?

Am I getting the stock at the right Valuation ?

Is the dividend yield, both in terms of percentage of earnings and absolute value, growing? ( Dividend Compounding ).

Is the company growing steadily, even if it’s at a slow pace? ( For Steal Deals).

How can one stay updated on dividend-yielding stock performance while minimizing ongoing monitoring efforts?

I don’t believe in adopting a “buy and forget” strategy for dividend-yielding stocks. While it is possible to reduce the amount of time spent on monitoring these stocks, complete disregard is not advisable.

Event-based monitoring is crucial. By staying informed through stock exchange filings and public news, one can obtain important information about the company as it happens. It is essential to dedicate some time to analyzing the impact of such events on the company and devising an exit plan if necessary.

Periodic monitoring is also important. The same fundamental questions I asked before buying the stock remain relevant. Therefore, I would review these aspects every six months and continue to stay invested as long as all indicators remain positive.

Finding a balance between reducing monitoring time and staying informed is key to effectively managing dividend-yielding stocks. By staying vigilant and periodically evaluating the company’s performance, one can make informed decisions while optimizing their investment strategy.

Summary.

Let me conclude this blog by leaving some intriguing thoughts in the minds of the readers.

Envision a day when your monthly expenses are effortlessly covered by the dividends you receive, providing you with financial security and peace of mind.

Envision a day when the company you invested in has experienced substantial growth over time, resulting in consistent dividends that match or even exceed the initial purchase price of your stocks.

Now, picture all of this unfolding after you retire from the traditional 9-5 job, allowing you to enjoy a fulfilling and worry-free lifestyle.

These possibilities demonstrate the potential power of smart investment decisions, strategic planning, and the long-term benefits that dividend stocks can offer. As you navigate your financial journey, consider the potential rewards that await you when you embrace the world of investing and make informed choices for your future.

Here’s the Comprehensive List of Our Blogs: Keep it Handy, Share with Friends and Family, Smash that Like Button, and Subscribe to Receive Blog Updates First. Your support fuels our passion for creating insightful content!

Disclaimer: This blog post is intended for informational purposes only and should not be considered as financial advice. Always conduct thorough research and consult with a qualified financial professional before making investment decision.

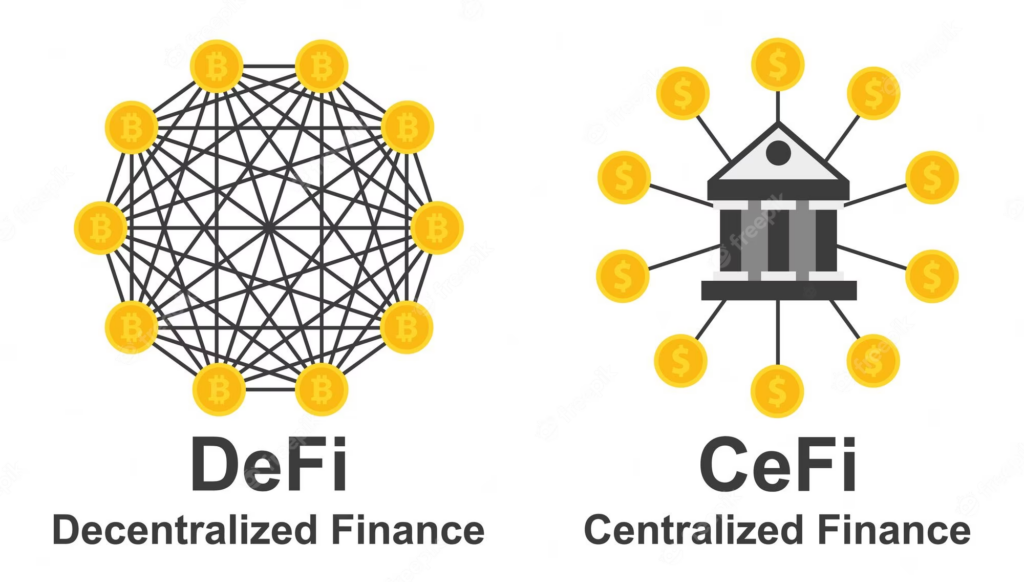

In a world filled with curiosity and controversy surrounding cryptocurrencies, few dare to delve into their intricacies. The complexity of this innovative digital realm often hinders understanding, leaving many hesitant to explore further. As a software and electronics engineer, I myself embarked on a challenging journey to comprehend its intricacies, and though I still have much to learn, I am eager to share my knowledge through a series of enlightening blogs. Welcome to the inaugural post, where we will begin by uncovering the genesis of cryptocurrencies and exploring the myriad advantages they bring to the table. Moreover, we will venture into the realm of traditional banking systems, unveiling the stark differences that set this groundbreaking solution apart.

Unmasking the Pitfalls: Common Issues with Conventional Banking Systems.

Soon after the 2008 economic crash, a group of forward-thinkers dared to question the safety of traditional banks as custodians of their hard-earned money. They yearned for a financial landscape beyond the confines of banking, driven by a desire for change. Let’s uncover the common pitfalls they identified, shedding light on the problems that led them to seek alternatives to traditional banking systems.

Banks had too much control: People felt that banks and governments had too much power over their money. They worried that this could lead to problems like censorship, freezing of accounts, or restrictions on accessing funds.

Privacy concerns: Traditional banks often required individuals to share personal information during transactions, which invaded their privacy.

Banks wereExpensive middlemen: Using banks for transactions often involved many middlemen, like banks, payment processors, and clearinghouses, which added extra costs. This was even more evident when there were international transactions taken up by people.

Simplified Access for everyone: Some people didn’t have access to traditional banks, especially in poorer areas.

Security and trust: There were concerns about fraud, hacking, and data breaches in traditional banking.

New possibilities: Cryptocurrencies opened up new ways of doing things in finance. They made it possible to create smart contracts, decentralized apps, and digital money that could change how we handle money and other financial activities.

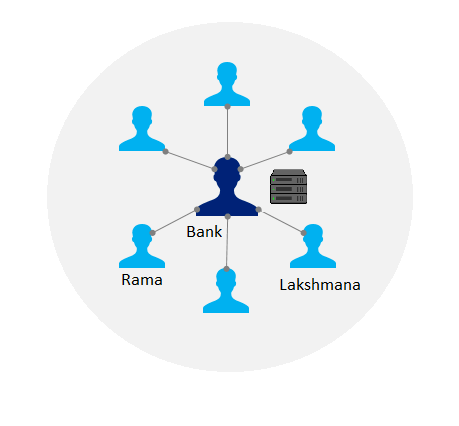

Exploring Traditional Transactions : Unveiling the Role of Banks in Conventional Financial Interactions

In this section, we will delve into the intricacies of conventional transactions facilitated by banks, shedding light on the fundamental processes involved. From initiating a transaction to its completion, we will examine the role of banks in facilitating financial interactions between individuals, uncovering the inner workings of the traditional transaction landscape.

Let’s consider a hypothetical transaction between Rama and Lakshmana as an example.

Agreement on Transaction: Lakshmana and Rama agree on the cost of the work done, and Rama wishes to pay Lakshmana the agreed amount of Rs.100/-.

Approach the Bank: Both Lakshmana and Rama visit the bank to initiate the transaction. They inform a bank representative about their intention to transfer funds from Rama to Lakshmana.

Providing Information: The bank asks Lakshmana and Rama to provide the necessary information, which typically includes their account details, identification, and transaction details (such as the amount and purpose of the payment).

Bank Server Entry: The bank representative enters the transaction details into the bank’s server. They perform three entries: deducting Rs 100/- from Rama’s account, adding the same amount to Lakshmana’s account, and deducting service fees of Rs 5/- from both accounts for the banking services rendered.

Transaction Completion: Once the entries are made, the transaction is considered complete. The funds are transferred from Rama’s account to Lakshmana’s account, and the bank deducts service fees for facilitating the transaction.

Key Points:

Personal Information: Banks require personal information from both parties to ensure the legitimacy of the transaction and comply with regulatory requirements.

Bank’s Authority: Transactions in the conventional system depend on the bank’s authority and involvement. They act as intermediaries and gatekeepers in the transfer of funds.

Service Fees: Banks charge service fees for providing their banking services, which are deducted from the involved parties’ accounts.

Concerns: This traditional process raises concerns related to privacy, reliance on centralized authority, and the cost associated with banking services.

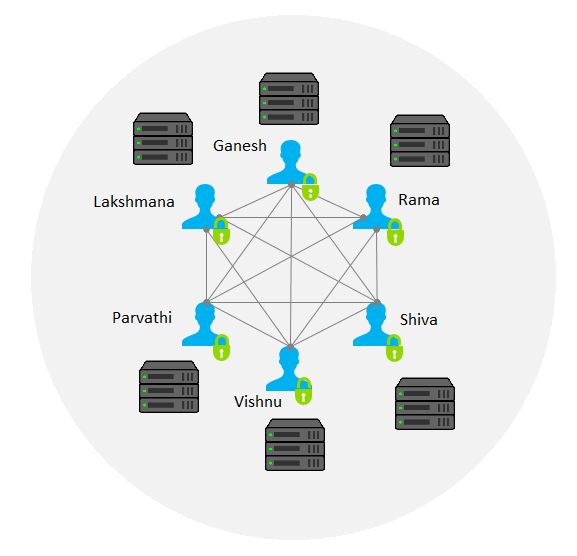

Exploring Decentralized Finance : Unveiling the technology under investigation.

Let’s consider the same hypothetical transaction between Rama and Lakshmana as an example to understand decentralized finance comparatively.

Decentralized Network: In a decentralized finance system, each participant (Rama, Lakshmana, Ganesh, Parvathi, Vishnu, Shiva ….) has their own server connected to a network. There is no Banker essentially at the center.

Transaction Intent: Rama, wanting to pay a specific amount Rs. 100/- to Lakshmana, publicly announces his intention to make the payment over the network. This announcement is visible to all participants.

Transaction Acceptance: Lakshmana, in response, publicly announces his acceptance of the specified amount Rs 100/- from Rama. This acceptance is also visible to all participants in the network.

Recording on Servers: All participants, including Rama and Lakshmana, record the transaction details on their respective servers. This creates a distributed ledger where multiple copies of the transaction record exist across different servers.

Transaction Confirmation: The network participants validate and verify the recorded transactions using consensus mechanisms such as proof-of-work or proof-of-stake. This ensures the accuracy and integrity of the transaction history.

Transaction Completion: Once the network reaches a consensus on the validity of the transaction, it is considered complete. The funds are effectively transferred from Rama to Lakshmana, and the transaction details are permanently recorded in the distributed ledger on each participant’s server.

Key Points:

Decentralized Network: Participants maintain their own servers connected to a global network, eliminating the need for a centralized authority like a bank.

Public Announcement: Transaction details are publicly announced to ensure transparency and visibility among network participants. In the real scenario there will be code names that shall be used by every customer so that the other people in the network do not know who the real person owning the account is.

Distributed Ledger: Transactions are recorded on multiple servers, creating a distributed ledger that is resistant to single points of failure or manipulation by one single person in the node.

Consensus Mechanism: Participants collectively verify and agree on the validity of transactions, typically through consensus algorithms, ensuring the integrity of the system.

No Transaction fee : It shall be observed that there is no transaction fee involved in this transaction by the middleman and also it is country agnostic.

While decentralized systems offer numerous benefits, they do present challenges that need to be considered.

It is not practical for everyone to have servers at their homes like banks in order to participate in decentralized networks. The requirement for individuals to set up and maintain their own servers poses challenges in terms of technical expertise, cost, and infrastructure. Many people may lack the necessary knowledge or resources to establish and manage servers effectively.

For non-tech-savvy individuals to engage with decentralized networks, user-friendly interfaces and simplified tools need to be developed. The user experience must be intuitive and accessible, eliminating the need for deep technical understanding. However, achieving this level of usability remains an ongoing challenge.

Another concern relates to potential misuse of decentralized systems. Since transactions are publicly recorded on the network, there is a perception that it could enable illegal activities, including money laundering. While decentralized systems prioritize privacy and security, they should also adhere to regulatory frameworks and address concerns related to illicit activities. Striking a balance between privacy and compliance is crucial for widespread adoption and acceptance of decentralized finance.

The Real Mystery : Who Feed these systems with money ? What is Cryptocurrency?

In the realm of decentralized finance, a crucial question lingers: Who breathes life into this groundbreaking system by injecting money? Unlike conventional banking, where governments play a central role (Sovereign), the origins of cryptocurrencies and their initial injection into the network are shrouded in intrigue.

Stay tuned for the upcoming blog, where we’ll delve into the captivating tale of how money finds its way into this revolutionary network. Don’t miss out on this eye-opening exploration! In the meantime, make sure to like, share, and spread the word about this blog to your friends and family.

Here’s the Comprehensive List of Our Blogs: Keep it Handy, Share with Friends and Family, Smash that Like Button, and Subscribe to Receive Blog Updates First. Your support fuels our passion for creating insightful content!

Disclaimer: This blog post is intended for informational purposes only and should not be considered as financial advice. Always conduct thorough research and consult with a qualified financial professional before making investment decision.

![Mutual Funds [Part 2] : Unveiling the Secrets of Goal-Oriented Fund Selection.](https://profitablepursuits.in/wp-content/uploads/2023/06/Mutual-Funds-2-825x510.jpg)