In today’s fast-paced world, financial literacy is more important than ever. Many of us were never taught about financial planning in school or by our parents, leaving us vulnerable to financial crises. If you’re one emergency away from bankruptcy, it’s time to take control of your finances. Here’s a straightforward guide to help you start your financial planning journey.

Step 1: Get Term Insurance

The first step in securing your family’s future is to get a term insurance policy. This is a cost-effective way to ensure that your loved ones are protected financially if something happens to you.

How Much Coverage Do You Need?

Use this formula to determine your total sum assured:

Total Sum Assured = ((Total Monthly Spend + EMI) / 50,000) * 1 Crore

This calculation ensures that your family can maintain their lifestyle even in your absence. Remember, you can discontinue this insurance once you have built a substantial financial cushion.

Step 2: Invest in Health Insurance

Medical emergencies can drain your savings faster than you think. A good health insurance policy protects you from unexpected medical expenses, allowing you to focus on growing your wealth.

Coverage Recommendations:

For Parents: At least ₹10 Lakhs per person.

For Yourself, Spouse, and Children: At least ₹5 Lakhs per person.

Don’t rely solely on employer-provided insurance. Create your own policy to avoid complications related to pre-existing conditions or waiting periods when switching jobs.

Step 3: Save Before You Spend

One of the simplest yet most effective financial habits is to save before you spend. Here’s how:

Open Two Bank Accounts:

Salary Account: Where your paycheck goes.

Savings Account: Transfer the necessary amount for EMIs and savings as soon as you receive your salary.

Spend What’s Left: Use the remaining balance in your salary account for your daily expenses. This method ensures that you prioritize savings and debt repayment.

Step 4: Plan for Retirement

A common rule of thumb is that for every ₹50,000 you need per month today, you will need ₹1 Crore at retirement. However, if you wish to maintain your current lifestyle, consider planning for ₹2 Crores for every ₹50,000.

Why the Increase?

As you age, your lifestyle may change, and inflation will affect your purchasing power. Observing your parents and in-laws can provide insight into the financial needs of retirement.

Step 5: The 15-15-15 Rule for Investing

Investing is crucial for building wealth. Here’s a simple rule to follow:

Invest ₹15,000 every month for 15 years.

Aim for a growth rate of 15% per annum.

By following this strategy, you could accumulate ₹1 Crore by the end of the investment period. Adjust your monthly investment based on your retirement goals and the number of Crores you need.

Where to Invest?

Achieving a 15% return is challenging but possible through well-researched mutual funds or direct equity investments. If you’re unsure, consider investing in index funds, which can provide a more conservative return of around 12%.

Conclusion

Financial planning may seem daunting, but taking these steps can help you secure your future and that of your family. Remember, I am not a certified financial planner or investment advisor; I am simply sharing lessons I’ve learned and practiced over time for educational purposes. Start your journey today, and take control of your financial destiny!

Here’s the Comprehensive List of Our Blogs: Keep it Handy, Share with Friends and Family, Smash that Like Button, and Subscribe to Receive Blog Updates First. Your support fuels our passion for creating insightful content!

Warren Buffett is renowned for his investment acumen and business prowess. But what about his personal finance wisdom? In this article, we’ll delve into some of his most insightful quotes and explore how middle-class Indians can apply them to achieve financial freedom.

Investing Wisely

Investing wisely means considering the long-term value of your investments rather than just focusing on the price. This is evident in Buffett’s quote “Price is what you pay. Value is what you get.” By prioritizing long-term growth over short-term gains, middle-class Indians can avoid market fluctuations and achieve greater returns.

Prioritising Saving and Investing

Buffett emphasizes the importance of prioritizing saving and investing first, then allocating the remaining funds for discretionary expenses. His quote “Do not save what is left after spending, but spend what is left after saving” highlights the need to make saving a priority and avoid overspending.

Embracing a Long-Term Perspective

Buffett’s philosophy on holding period is reflected in his quote “Our favorite holding period is forever.” This emphasizes the importance of embracing a long-term perspective and avoiding frequent trading. By adopting a buy-and-hold approach, middle-class Indians can weather market volatility and achieve greater returns over time.

Considering Index Funds

Index funds offer an excellent way to diversify your portfolio and minimize fees. Buffett’s quote “It’s far better to do something via an index fund than to get swindled” highlights the importance of considering low-cost index funds for diversified portfolio management.

Focusing on Compound Interest

Compound interest can be a powerful force in growing your wealth over time. Buffett’s quote “You only have to do very few things right in your lifetime to be remembered” emphasizes the importance of focusing on compound interest and letting it work for you over time.

Avoiding Emotional Decision-Making

Investments should not define one’s identity or create undue stress. Buffett’s quote “Someone’s stock portfolio is not their life” highlights the need to avoid emotional decision-making and maintain a rational approach to investing.

Staying Informed but Not Getting Caught Up in Hype

Finally, Buffett’s quote “The game is afoot” emphasizes the importance of staying informed about personal finance and investing concepts without getting caught up in market trends or hot new investment products. It’s essential to maintain a long-term perspective and focus on your financial goals.

Conclusion:

By applying these principles from Warren Buffett’s personal finance wisdom, middle-class Indians can develop a strong foundation for achieving their financial goals and securing their future. By prioritizing saving and investing, embracing a long-term perspective, considering index funds, focusing on compound interest, avoiding emotional decision-making, and staying informed but not getting caught up in hype, individuals can build wealth over time and achieve greater financial freedom.

Growing up, I was fortunate to have parents and relatives who instilled in me the value of saving and equipped me with the tools to do so. Their guidance not only shaped my financial habits but also spared me from the precarious hand-to-mouth existence that many find themselves in month after month. Reflecting on this, I can’t help but feel immensely fortunate.

Yet, I also find myself pondering a perplexing question: why aren’t such fundamental life skills taught in schools? In a country like India, discussions about money are often treated as taboo subjects in educational institutions. Whether this omission is unintentional or deliberate is a matter open to debate. Perhaps it stems from a desire to foster a spending-driven economy, one that prioritizes showcasing GDP growth and economic prowess to the world.

Regardless of the reasons behind this educational gap, I’ve made a personal commitment to ensure that my child, and anyone else willing to listen, receives the financial education that our schooling system overlooks. Through this blog, I aim to share the framework that I believe is the cornerstone of a solid financial education for children.

This framework, inspired by the teachings of my grandparents, parents, and countless books on personal finance, serves as a blueprint for nurturing financial literacy from a young age. By summarizing and elucidating this framework here, my hope is that readers—parents like myself, who may have felt unequipped to tackle this subject—can adapt it to their own needs and set their children on a path towards financial empowerment. Join me as we embark on this journey to equip the next generation with the tools they need to navigate the complexities of personal finance with confidence and competence.

Step 1 : Introduce a Personalised Piggy Banks at Age 3.

At the age of 3 or so, gift your child a piggy bank that is visually appealing and engaging to them, not just what the parents prefer. Choose a piggy bank design that aligns with your child’s interests and personality, whether it’s a favorite cartoon character, animal, or vibrant color. Making the piggy bank personalized and fun will help spark their interest in saving money from an early age. This hands-on tool can serve as the foundation for teaching basic financial concepts through interactive play and setting savings goals. Starting with a piggy bank they genuinely enjoy using can make the process of learning about money management more enjoyable and impactful for young children.

To instill the habit of saving in your child, regularly give them any spare coins or small denomination notes to deposit into their piggy bank. Encourage them by explaining that once the piggy bank is full, they can use the saved money to buy something they truly desire. When your child requests a toy or item, teach them patience by suggesting they wait until the piggy bank is full to make the purchase with their own savings. Additionally, on days when your child displays exceptional behavior, reward them with a little extra money to add to their savings, reinforcing the connection between good behavior and positive outcomes. This approach not only teaches financial responsibility but also cultivates patience, delayed gratification, and the value of hard-earned money in a practical and rewarding manner.

As your child’s piggy bank starts to fill up with savings, make it a point to involve them in your regular shopping trips. When you go to the supermarket or other stores, hand the money over to your child and have them pay the merchant directly. This hands-on experience allows them to see the process of exchanging money for goods and services. Once you get home, take the time to discuss the event with your child. Help them understand that money is required to purchase the items you need, reinforcing the connection between saving, spending, and obtaining the things you want or require. This real-world practice, combined with the follow-up conversation, can solidify your child’s grasp of basic financial concepts in a meaningful, engaging way.

Make it a point that kid gets a chance to buy what ever it wants with very limited or no restrictions.

Step 2 : Introducing the ‘Co-Pay Model’: Teaching Kids Financial Responsibility Through Shared Costs at Age 5.

When your child reaches the age of 5, consider transitioning from a full-pay model to a cost-sharing approach for purchases. Whenever your child requests a toy or other item, ask them to contribute 5-10% of the cost from their piggy bank savings. This teaches them the value of money and the importance of prioritizing their spending. Reinforce the lesson by refusing to buy the item if their piggy bank is empty, encouraging them to save up for the desired purchase.

At the same time, avoid over-gifting money to your child. Instead, provide additional funds as rewards for positive behaviors, such as helping to clean their room, making their bed, or going a day without screen time. This ties financial rewards to good habits, further instilling the connection between responsible actions and financial benefits. By transitioning to a cost-sharing model and selectively rewarding desired behaviors, you can continue building your child’s financial literacy and money management skills as they grow older.

In the copay model of teaching delayed gratification to children, it is essential to emphasize the importance of delayed gratification in relation to the size of the purchase. By linking the copay percentage to the ticket size of the item they desire, children can better grasp the concept of delayed gratification. When the copay percentage increases with larger purchases, children learn that patience and saving are required for more significant rewards. This approach not only reinforces the value of self-control and discipline but also teaches children the correlation between delayed gratification and achieving more substantial goals. By adjusting the copay percentage based on the cost of the desired item, kids can develop a deeper understanding of delayed gratification and the rewards that come with patience and long-term planning.

Step 3 : Bring out the little Entrepreneur at Age 8.

Encouraging children to develop new skills and turn them into products or services they can sell is a powerful way to build their financial literacy and entrepreneurial mindset. This approach aligns with the philosophy espoused by Naval Ravikant – “Learn to Sell, Learn to Build. If you can do both, you will be unstoppable.”

Start by helping your child identify their interests and talents. Perhaps they enjoy making colorful paintings or have a knack for crafting homemade soaps. Provide them with the necessary resources and guidance to turn these hobbies into small business ventures. Teach them how to source materials, create their products, and market them to friends, family, and the local community.Leverage online resources to inspire your child and provide them with ideas.

Explore stories of other smart, young entrepreneurs who have found success through their creativity and determination. This exposure can spark their imagination and motivate them to think beyond traditional ways of earning money and save them in the piggy bank and involve in the co-pay model.

Encourage your child to experiment, learn from failures, and continuously iterate on their business ideas.By empowering your child to become a young entrepreneur, you are not only fostering their financial literacy but also instilling valuable skills such as problem-solving, critical thinking, and the ability to turn their passions into profitable ventures. This holistic approach to personal finance education can set your child up for long-term success, both financially and in their overall personal development.

Step 4 : Transitioning from Piggy Bank to Formal Banking at Age 12.

As your child’s savings in the piggy bank grow, it’s time to introduce them to the formal banking system. Open a bank account in their name and transfer the accumulated funds from the piggy bank. Take your child to the bank counter and have them personally hand over the money to the teller for deposit. This hands-on experience will help them understand the process of depositing funds into a bank account.

Explain the entries made in the passbook, showcasing the balance and any deposits made. When it’s time to make a withdrawal, repeat the process, allowing your child to interact with the teller and observe the updated balance. Emphasize the importance of this record-keeping, as it helps them track their savings.

As your child begins to deposit their savings into a formal bank account, introduce them to the concept of interest. Explain that the bank pays them a small percentage, known as interest, for keeping their money in the account. This interest is credited to their account on a regular basis, typically monthly or quarterly.Encourage your child to closely monitor the “Interest” line item in their passbook.

Explain the simple interest calculation, where the interest earned is a function of the principal amount, the interest rate, and the time period. Invite them to calculate the interest themselves, fostering a deeper understanding of how their savings can grow over time.Furthermore, discuss the bank’s perspective – how they utilize the deposited funds to generate their own revenue, and why they are willing to share a portion of that with account holders in the form of interest. This will help your child appreciate the mutually beneficial relationship between the bank and the account holder, setting the stage for more advanced financial concepts in the future.

After your child has become comfortable with the basic savings account, introduce them to more advanced banking products like recurring deposits (RDs) and fixed deposits (FDs). Explain that an RD allows them to set aside a fixed amount of money at regular intervals, typically monthly, to grow their savings systematically.Guide your child through the process of opening an RD account, emphasizing the importance of consistent contributions. Demonstrate how the interest earned on an RD is typically higher than a regular savings account, rewarding their disciplined saving habits. As the RD matures, have your child withdraw the funds and observe the total amount, including the interest earned.

Building on this experience, introduce the concept of a fixed deposit (FD). Explain that an FD allows them to deposit a lump sum of money for a predetermined period, usually ranging from a few months to several years. Highlight how FDs generally offer even higher interest rates compared to RDs, as the bank can rely on the funds being unavailable for a longer duration. Encourage your child to allocate a portion of their savings into an FD, reinforcing the idea of diversifying their financial portfolio.

By guiding your child through the transition from a basic savings account to more sophisticated banking products, you are equipping them with a comprehensive understanding of how to grow their wealth through various savings and investment strategies.

Summary :

In this blog post, we explored a comprehensive approach to teaching kids about personal finance, starting from a young age with the introduction of a piggy bank and gradually transitioning to formal banking. By involving children in real-world transactions, encouraging savings, and introducing them to banking products like recurring deposits and fixed deposits, parents can instill valuable financial literacy skills and cultivate an entrepreneurial mindset in their children. Understanding the concepts of interest, delayed gratification, and the importance of consistent saving lays a strong foundation for children to make informed financial decisions and build a secure financial future.

Here’s the Comprehensive List of Our Blogs: Keep it Handy, Share with Friends and Family, Smash that Like Button, and Subscribe to Receive Blog Updates First. Your support fuels our passion for creating insightful content!

Disclaimer: This blog post is intended for informational purposes only and should not be considered as financial advice. Always conduct thorough research and consult with a qualified financial professional before making investment decision.

Introduction: Lost in the Race, Forgotten ‘Enough’.

In the relentless pursuit of wealth, we find ourselves caught in the rat race, often forgetting to pause and ask a fundamental question: how much is truly enough? Reflecting on my own journey, I recall that as a child, I believed having 10 lakhs would make life heavenly. However, with time, my aspirations escalated; from dreaming of 1 crore, I eventually aimed for 100 crores, influenced by societal notions of luxury. Reading “The Psychology of Money” by Morgan Housel unveiled a universal truth – this desire for more is an endless cycle. Even the wealthy yearn for greater wealth: Michael Jordan eyes Jeff Bezos, and Bezos eyes Elon Musk.

In a moment of contemplation, a lingering question emerged within me: “What is the threshold of sufficiency?” Turning to the wisdom of my guru, Acharya Chanakya, I discovered his profound insight: “

the moist important thing for a happy life is satisfaction. If you are satisfied with life then there will be no problem in your life.”To be satisfied , one must know how to control his senses. No one is happier than the person who is satisfied by controlling his senses.”

Thus began my quest to explore the concept of “enough.”

The Cost of Chasing More: Tragedies Unveiled.

Conversations with my friends opened my eyes to some harsh realities. One friend had spent ten years building up money, but lost it all in just a few months by trading in ways that were very risky. He was convinced by his colleagues that he could make more money quickly by trading instead of saving for a small piece of land.

Another friend shared that their family ran a chit fund, but things went wrong and they lost all the money they were taking care of for others. This led them to bankruptcy.

While growing up, I saw many people from lower middle-class families lose everything because they hoped to get rich quickly. They gambled all their money, even the little they had, just to avoid the shame of being broke.

My own family also struggled with money. We had times when we had to walk a long way to save a small amount of money, just to buy a simple snack.

Seeing all of these situations shaped how I handle money. It made me wonder: Is it really worth it to chase after money so much that we lose out on life, time for ourselves, and our self-respect?.

Purpose and Passion: The Dual Pathways of Life.

As we progress through life, our selection of business or profession naturally transforms. For certain individuals, their work becomes a channel through which they find a profound sense of purpose and fulfillment. However, contrasting this, there are those who find themselves trapped in roles that bring about dissatisfaction and resentment.

Irrespective of the specific circumstances, the notion of constructing a financial corpus gains paramount importance. This corpus serves as a reservoir of financial resources, a reservoir that is integral to attaining a state of financial independence. This state liberates individuals from the compulsion to work solely for monetary gain, thereby affording them the luxury to delve into their passions and interests with unbridled enthusiasm.

In essence, the strategic accumulation of wealth doesn’t solely cater to material acquisitions, but rather, it acts as a conduit to a more profound form of freedom. This freedom extends beyond merely quitting a disliked job; it empowers one to explore their innate potential, nurture their creative endeavors, and lead a life aligned with their true aspirations.

Unleashing the Potential: The Miraculous 2 Crore Corpus.

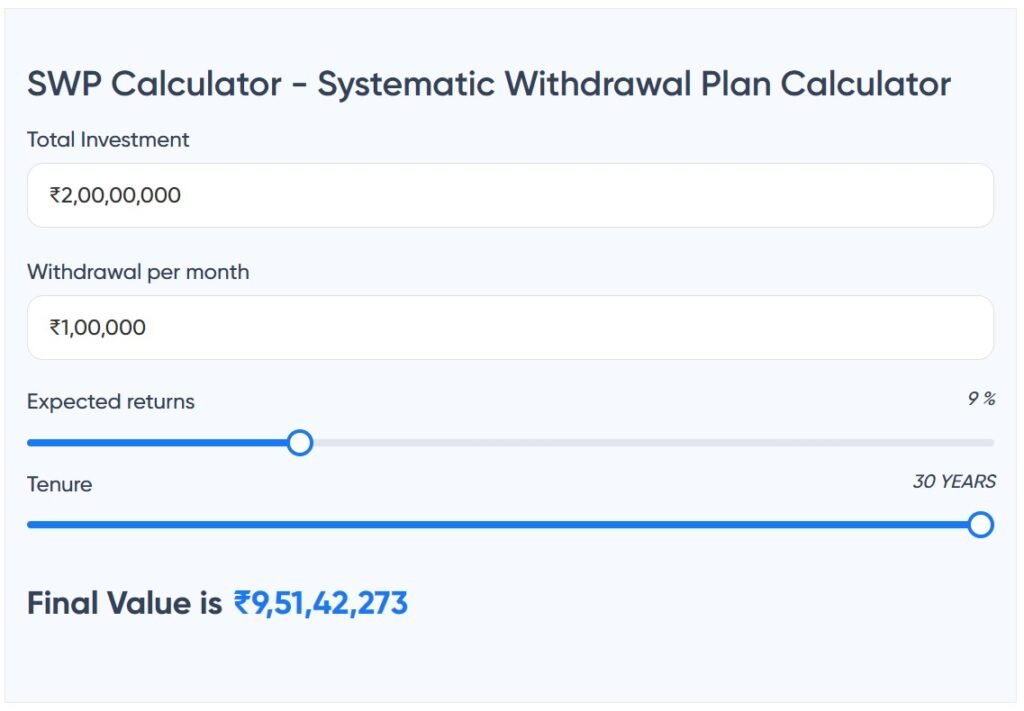

Let’s consider a scenario where an individual, through ethical means, manages to accumulate 2 crores in their business or profession. Imagine this sum being invested in an Indian index fund, which hypothetically yields a 9% year-on-year return (being conservative here, considering that historically NIFTY has averaged 12%). Suppose this person withdraws 1 lakh every month for 30 years, allowing the remainder to continue compounding. Surprisingly, at the end of these 30 years, the corpus would still amount to a substantial 10 crores!

This prompts us to question: do we truly require such a substantial amount of money? With age, our need for extravagant luxury often diminishes. By having comprehensive health insurance in place, monthly expenses could be significantly reduced.

After conducting this thought experiment, I found myself taken aback and pushed to delve deeper. Could I realistically aim to amass 2 crores and attain a form of financial independence? Certainly, this wouldn’t imply ceasing work, but rather, it would infuse a heightened sense of confidence and contentment into life. Wouldn’t that be a valuable achievement?

I’m not certain if 2 crores is “The” figure that applies to me. What I wish to emphasize to the reader is that each individual should take a pen and paper to ascertain this number. Without doing so, breaking free from the rat race can seem nearly impossible.

Upon reaching the juncture where our accumulated corpus is capable of consistently generating the desired monthly revenue while also undergoing substantial compounding, a pivotal decision arises. This crossroads invites us to consider bidding farewell to the professions that evoke our disdain or the jobs that no longer kindle our interest. The financial security provided by the self-sustaining corpus can empower us to relinquish roles that once held us captive in the pursuit of monetary gains, paving the way for new chapters aligned with our genuine passions and aspirations. This transition signifies a transformative shift from obligation to choice, from the compulsion of necessity to the liberation of fulfillment.

Dharma’s Light: Transforming Desires into Destiny.

Here come the natural question how do i find my passion?

Well its not that easy to answer , but not difficult either …

I can only quote some awakening links from the Sanathana Dharma.

Dharma is your unique purpose in life. It is the process by which you use your unique skills and passions to serve your community and the world.

There is a phrase in the Upanishads, one of the great Indian texts, that says:

” You are what your deepest desire is,

As is your desire, so is your intent,

As is your intent, so is your will,

As is your will, so is your deed,

As is your deed, so is your destiny. “

Wisdom from Mahabharata: Navigating the Battle Within for a Noble Life.

As we embark on the quest to discover a meaningful purpose for our lives, it’s crucial to bear in mind the insightful encapsulation of the Mahabharata by a wise individual:

“Mahabharata in a metaphorical way: the battle of Mahabharata is, actually, the battle between the good and evil present in ourselves; this means that we are composed out of forces of evil and of good. Our mental condition is not void: forces of evil and of good are present in us. Therefore, we cannot wait and see: we ought to take a decision on our moral constitution.”

Here’s the Comprehensive List of Our Blogs: Keep it Handy, Share with Friends and Family, Smash that Like Button, and Subscribe to Receive Blog Updates First. Your support fuels our passion for creating insightful content!

Disclaimer: This blog post is intended for informational purposes only and should not be considered as financial advice. Always conduct thorough research and consult with a qualified financial professional before making investment dec

Growing up in a middle-class household, I witnessed my father’s relentless struggle to repay loans, and his lifelong dream of owning a car remained perpetually postponed. This experience instilled in me a profound understanding of the perils of debt and the value of delayed gratification. Guided by my parents’ wisdom, I embarked on a personal journey, determined to save diligently and patiently work towards my goal of owning a car at the opportune moment. In this blog, I share my inspiring tale of transforming a wish into reality, demonstrating how embracing delayed gratification can lead to a brighter future.

Navigating the Temptation: My Journey from FOMO to Financial Wisdom.

As I entered the realm of adulthood and started my professional journey, it seemed as though everyone around me was eagerly booking cars, flaunting their newfound mobility through convenient EMIs. Feeling a sense of FOMO (Fear Of Missing Out), I began to question whether I was making a mistake by not following suit. The allure of owning a car consumed my thoughts, and I couldn’t help but imagine the joy and pride it would bring to my family and myself. However, my innate sense of financial responsibility urged me to pause and evaluate the situation before making any impulsive decisions.

Recognizing the need for clarity, I delved into research, armed with calculators and determination. I sought to understand the intricacies of car financing and the true implications of taking on EMIs. Through careful analysis, I discovered that these seemingly attractive monthly payments came bundled with long-term commitments and interest accruals. It became apparent that a hasty decision could potentially lead me down the same arduous path my father had faced. With renewed resolve, I chose a different course, one that required patience and delayed gratification. In the following sections, I share the invaluable insights I gained along the way and how they ultimately guided me towards a smarter, more sustainable approach to owning my dream car.

The Harsh Reality: Counting the True Costs of Car Ownership.

In my determined pursuit of owning a car, I delved into detailed research, only to be confronted with a stark reality. After careful calculations, it became apparent that I would need to exhaust a significant portion of my savings accumulated over 2-3 years, while also adopting a frugal lifestyle, just to afford a basic car. The financial strain didn’t stop there. When considering the costs of maintenance, it became clear that an additional 2-3 months of savings would be required each year. Moreover, the anticipated fuel expenses, which would quadruple in comparison to my current motorcycle usage, added yet another burden. The enormity of these expenses painted a clear picture, forcing me to acknowledge the unfeasibility of my dream and challenging my resolve to resist the tempting allure of car ownership.

Overwhelmed by sadness and disillusionment regarding my car ownership aspirations, my mother became my guiding light during those difficult times. She helped me realize that succumbing to peer pressure and impulsive decisions was unnecessary. Drawing from my past experience of patiently saving for a computer, my mother instilled in me the belief that waiting was not only acceptable but also wise. With her guidance, I understood that as my income and savings grew over time, I would eventually be able to fulfill my dream of owning a car. Embracing this newfound clarity, I made a firm decision to wait until I had saved twice the necessary amount, empowering myself with financial security and a well-planned approach.

From Forgotten Dream to Driving Enthusiasm: Rediscovering the Joy of Car Ownership.

As I focused on saving money without a specific goal in mind, the once-burning desire to own a car gradually faded away. I grew accustomed to traveling by bus and train, finding contentment in the companionship of my trusty motorcycle, which had accompanied me on countless journeys spanning over 50,000 kilometers. It seemed as though my dream of car ownership had slipped into the depths of my memory. However, a pivotal moment occurred when I realized the importance of knowing how to drive. Witnessing the consequences of relying solely on a single driver during a late-night accident with my friends, I felt compelled to acquire the skill of driving. Enrolling in a nearby driving school, I swiftly learned the art of driving and embraced the opportunity to drive whenever friends were kind enough to share their cars, disregarding my initial lack of expertise behind the wheel.

After six years of working and embarking on various journeys, including trips to different countries, the time had come for me to start a new chapter in life—marriage. Seeking guidance, I turned to a wise and self-made man in his late 60s, who happened to be a father figure to one of my friends. During our conversation, he emphasized the importance of owning a car, not for the purpose of showing off, but to provide comfort to my family and as a reward for their unwavering support in raising me. He explained that having a car would be beneficial for visiting relatives in different cities for the wedding, taking my wife on outings outside the city, and ensuring the safety of a future child. Moreover, he reminded me that I had saved a considerable amount of money, even after considering the expenses of the wedding. Inspired by his wise counsel, I resolved to delve deeper into the matter and make an informed decision.

On the Road to Fulfillment: Unveiling My Dream Car and Making My Most Expensive Purchase.

Determined to make an informed decision, I embarked on a thorough exploration of the car market. Seeking advice from friends, conducting extensive online research, and visiting multiple showrooms, I meticulously compared various options. It became evident that to own a car meeting my requirements, I would need to allocate a budget of at least 8 Lakhs. Additionally, I learned that an annual expense of around 10,000 rupees for maintenance was a reasonable expectation. Armed with this knowledge and reassured by the fact that I had saved twice the required amount, I confidently proceeded with my choice. I made the decision to book an elite i20 from Hyundai, opting to pay the entire sum upfront in cash. Little did I know at the time that this purchase would become the most significant and expensive investment I had made up until that point in my life.

Despite having enough cash reserves for purchasing my dream car, a portion of it was tied up in Fixed Deposits. However, my father came forward with a generous offer, willing to share his savings and allowing me to repay him once the Fixed Deposits matured. This heartfelt gesture filled me with immense happiness, as it indicated that my family was not only supportive but also excited about having a car at home. Their willingness to contribute towards my dream further solidified my decision and deepened my sense of gratitude.

Creating Lifelong Memories: Our Journey of Adventure and Prioritizing Car Upgrades.

The joy of traveling together as a family in our beloved car has been unparalleled. Every journey we undertake becomes an opportunity to create precious memories that will be cherished for a lifetime. Whether it’s exploring serene hill stations, relaxing by picturesque beaches, or discovering cultural landmarks, our car has been the vehicle that has brought us closer as a family. The laughter, conversations, and shared experiences during these trips have strengthened our bond and created a sense of adventure that resonates with each member of the family. As we navigate through the winding roads and scenic routes, we have come to appreciate the true value of owning a car, beyond its mere functionality, as it becomes a vessel for our collective experiences and moments of pure joy.

As time goes by, we have begun to consider certain upgrades to our car to further enhance our travel experiences. One feature we desire is an automatic transmission, which would provide us with a smoother and more comfortable driving experience, particularly during congested city traffic. It would alleviate the constant engagement of the clutch and lessen strain on our legs, making our journeys more enjoyable and less tiring. Additionally, we have contemplated the inclusion of a sunroof in our car, especially for drives through the mesmerizing Western Ghats. The panoramic view it would offer, with sunlight streaming in and a clear view of the picturesque surroundings, would make our trips even more captivating and memorable for our son, who has developed a love for the beauty of nature. However, despite these desires, we have firmly decided to adhere to our original intention of waiting until we have at least five compelling reasons before considering another car purchase. This commitment ensures that our decisions are rooted in practicality and align with our family’s priorities, ensuring that each upgrade brings meaningful value to our lives and enriches our journeys even further.

Summary:

In this blog, I share my journey of delayed gratification in realizing my dream of owning a car. Despite being tempted by friends’ car purchases, I chose to postpone mine due to financial considerations. Through careful research and financial planning, I eventually purchased an elite i20, making it my most significant investment at the time. Alongside creating lasting memories and desiring certain car upgrades, I remain committed to waiting until there are compelling reasons for another purchase, staying true to the power of delayed gratification. This journey highlights the importance of thoughtful decision-making and the joy that comes from shared experiences with family.

Here’s the Comprehensive List of Our Blogs: Keep it Handy, Share with Friends and Family, Smash that Like Button, and Subscribe to Receive Blog Updates First. Your support fuels our passion for creating insightful content!

Disclaimer: This blog post is intended for informational purposes only and should not be considered as financial advice. Always conduct thorough research and consult with a qualified financial professional before making investment decision.

Dividends, the distributions of a portion of a company’s earnings to its shareholders, play a crucial role in the financial landscape. In this section, we will explore the concept of dividends and delve into the reasons why companies choose to pay them out. Understanding dividends is essential for investors seeking stable income streams and long-term wealth accumulation.

Why do companies choose to pay Dividend to Investors ?

Dividends represent a portion of a company’s profits that is shared with its shareholders. By paying dividends, companies reward their shareholders for their investment and participation in the company’s growth. This practice is not only a means of showing appreciation but also a strategic move to attract investors by offering an incentive beyond capital appreciation. Dividends can be a sign of a healthy and well-established company, instilling confidence in investors and attracting long-term shareholders.

In the above example, it can be observed that the company has consistently earned money year over year (YOY) and distributed dividends to investors, amounting to over 30-40% of its annual earnings. The remaining earnings are retained in the company’s balance sheet for reinvestment and further growth.

Consistent dividend payments distinguish good companies, while the mark of great companies lies in their consistent dividend increases over time. By maintaining a reliable dividend payout, good companies demonstrate their commitment to rewarding shareholders. On the other hand, great companies exhibit their exceptional financial strength and growth potential by consistently raising dividends, showcasing their ability to generate sustainable profits and create long-term value for investors

Why should one consider dividend yielding stocks in their portfolio?

If you had purchased TCS shares at Rs.140/- in the middle of 2005 and held onto them until now, not only would the stock have risen to Rs.3500/-, but you would by now also have started receiving approximately Rs.50/- per year as dividends.

Power of Dividend for long term investors.

Dividend Compounding : Investing in the right company and holding onto the shares for an extended period can yield remarkable results. Imagine purchasing shares of a company today at Rs.100 /- and remaining invested as the company grows and prospers over the decades. In such a scenario, it is entirely possible that after a few decades, you could receive an annual dividend of Rs.100 /- for each share you own, in addition to the substantial appreciation in the share price that occurred over the years.

During the stock market crash caused by COVID, had you purchased Karnataka bank stocks at Rs.35/-, you would now be receiving Rs.4/- or more as dividends every year, according to their dividend policy. This would represent a return of over 10% annually, excluding any potential stock price appreciation.

Buying Dividend yielding stocks at the right time.

Steal Deals: Dividends are not solely a long-term game; they also provide short-term opportunities for investors to achieve attractive yields. By making astute stock purchases at opportune moments, it is possible to generate returns that surpass traditional fixed deposit rates within a few years. With dividends often increasing over time as companies expand, investing in dividend-paying stocks presents the potential for substantial returns that go beyond long-term strategies. This dynamic nature of dividends allows investors to benefit from both short-term income and long-term growth, making them a compelling option for maximizing investment gains.

What factors do I considered when determining the appropriate allocation of dividend yielding stocks in my portfolio?

Dividend income can play a crucial role in retirement planning ( This need not be at 60 but when planned well can happen much earlier ). As individuals approach retirement from their 9 to 5 job , they often seek stable and reliable sources of income to support their lifestyle. Dividends can provide a steady stream of passive income, as many companies distribute a portion of their earnings to shareholders on a regular basis. This dividend income can serve as a valuable addition to other retirement income sources.

By investing in dividend-paying stocks or funds, retirees can potentially enjoy a consistent cash flow that helps cover living expenses and maintain financial security throughout their retirement years. Additionally, dividend income can offer a hedge against inflation, as many companies increase their dividend payouts over time, helping retirees preserve the purchasing power of their income. Overall, incorporating dividend income into retirement planning can provide retirees with a reliable and potentially growing source of funds to support their post-career lifestyle.

Some of the key elements I consider before adding dividend stocks to my portfolio.

While my main focus is on growth stocks, I’m open to attractive dividend yields in the market, such as the Karnataka bank example mentioned earlier. A balanced approach, combining both growth and dividend-yielding stocks, can optimize portfolio returns.

I believe that dividend-yielding stocks are more suitable for retirement planning, and I do not think it is advisable to add a significant number of dividend stocks to my portfolio early in my career. Doing so could potentially limit the growth potential of my capital.

Even during retirement, I don’t believe in allocating all my funds to dividend-yielding stocks. I understand that the decision to distribute dividends lies solely with the board of the company, and as a shareholder, I have no direct control over it. Dividend-yielding stocks form only a partial portion of my portfolio. For the remaining portion, I prefer investing in corporate bonds and fixed deposits.

What strategies or methods I employ to identify dividend yielding stocks?

Whether I’m investing for stock price appreciation or dividends, the fundamental checks I perform remain largely unchanged. However, when it comes to dividend-yielding stocks, there are certain liberties and considerations I take into account.

Will the products that the company is selling today still be in demand after a decade?

Does the company have a policy that mandates the payment of dividends during the normal course of business?

Has the company consistently paid out dividends in the past?

Are the company’s financials healthy – company shall pay dividend from its free cash flow and not via debt or equity dilution?

Are the promoters clean?

Am I getting the stock at the right Valuation ?

Is the dividend yield, both in terms of percentage of earnings and absolute value, growing? ( Dividend Compounding ).

Is the company growing steadily, even if it’s at a slow pace? ( For Steal Deals).

How can one stay updated on dividend-yielding stock performance while minimizing ongoing monitoring efforts?

I don’t believe in adopting a “buy and forget” strategy for dividend-yielding stocks. While it is possible to reduce the amount of time spent on monitoring these stocks, complete disregard is not advisable.

Event-based monitoring is crucial. By staying informed through stock exchange filings and public news, one can obtain important information about the company as it happens. It is essential to dedicate some time to analyzing the impact of such events on the company and devising an exit plan if necessary.

Periodic monitoring is also important. The same fundamental questions I asked before buying the stock remain relevant. Therefore, I would review these aspects every six months and continue to stay invested as long as all indicators remain positive.

Finding a balance between reducing monitoring time and staying informed is key to effectively managing dividend-yielding stocks. By staying vigilant and periodically evaluating the company’s performance, one can make informed decisions while optimizing their investment strategy.

Summary.

Let me conclude this blog by leaving some intriguing thoughts in the minds of the readers.

Envision a day when your monthly expenses are effortlessly covered by the dividends you receive, providing you with financial security and peace of mind.

Envision a day when the company you invested in has experienced substantial growth over time, resulting in consistent dividends that match or even exceed the initial purchase price of your stocks.

Now, picture all of this unfolding after you retire from the traditional 9-5 job, allowing you to enjoy a fulfilling and worry-free lifestyle.

These possibilities demonstrate the potential power of smart investment decisions, strategic planning, and the long-term benefits that dividend stocks can offer. As you navigate your financial journey, consider the potential rewards that await you when you embrace the world of investing and make informed choices for your future.

Here’s the Comprehensive List of Our Blogs: Keep it Handy, Share with Friends and Family, Smash that Like Button, and Subscribe to Receive Blog Updates First. Your support fuels our passion for creating insightful content!

Disclaimer: This blog post is intended for informational purposes only and should not be considered as financial advice. Always conduct thorough research and consult with a qualified financial professional before making investment decision.

Stage 1 : A Personal Account of Manipulation and Harrowing Consequences with Credit Cards.

In a chilling story shared by my father, I discovered the nightmarish experience he endured with a credit card and the manipulation he faced from his own brother. It was a distressing account of how his brother forced him to get a credit card, only to exploit it for personal gain. The consequences were severe, and the relentless actions of debt collectors left a lasting impact on our family, profoundly influencing my perspective on credit cards.

As my father recounted the troubling events, I couldn’t help but feel deep empathy and a strong desire to protect myself from a similar situation. Hearing about the mounting debts, the financial burden, and the relentless harassment he faced, I made a firm commitment to never venture down that dangerous path. This cautionary tale served as a powerful reminder of the potential risks associated with credit cards, motivating me to approach my own financial journey with utmost caution and mindfulness.

Stage 2 : Credit Cards turned out to be Essential Partners in Early Travel Adventures

Paragraph: When I first embarked on my journeys abroad, I quickly realized that credit cards played a vital role in making travel arrangements. Even a simple international call from the airport to let my parents know I had arrived safely required a credit card. As online booking platforms gained popularity and digital payments became more common, having a credit card became a requirement for securing flights, accommodations, and other travel services.

In those early days of traveling internationally, credit cards became indispensable companions. They made transactions seamless and provided a sense of security during uncertain trips. Credit cards opened doors to new experiences, offering convenience and opportunities that were hard to ignore. Despite their downsides, credit cards were essential tools in navigating the initial stages of my travel adventures.

But I still did not get one for myself; I lived by borrowing others’ cards and repaying them immediately with cash.

Stage 3 : Eye-Opening Conversations: Unveiling the Allure of Credit Cards during a Memorable Trip

During a memorable trip to Osaka with friends, the topic of credit cards came up one night, leading to eye-opening conversations. A friend excitedly shared how lucrative the point system of his credit card was, boasting about the expensive items he had obtained for free, such as a passport holder, a leather travel bag, and even Ray-Ban glasses. Another friend chimed in, explaining how he strategically managed two credit cards, balancing their billing cycles to always have a surplus of money available without any cost. Lastly, another friend recounted a crucial moment when his mother fell ill, leaving him in a desperate situation. With no immediate funds, the hospitals were hesitant to provide further care. Fortunately, he had a credit card that came to his rescue, allowing him to promptly cover the expenses. Hearing these stories compelled me to delve deeper into the world of credit cards, igniting a curiosity about owning one for myself.

Stage 4 : My Credit Card Journey: From Research to Frustration and Lessons Learned.

After consulting friends and exploring credit cards from various banks, I stumbled upon an enticing moneyback card from HDFC. With its appealing features like zero annual maintenance, lifetime free card, and earning 1 point for every 100 spent, I decided to order one online. Soon, my phone buzzed with calls from various banks, offering tempting deals. However, staying true to my research, I stuck to my initial choice. From that point forward, my focus shifted to understanding the intricacies of credit card statements, deciphering billing cycles, total due amounts, and minimum payments. By ensuring timely payments, I successfully avoided penalties and maintained a spotless record.

As a thrifty spender, I discovered that the points earned from my HDFC card were not as lucrative as expected. Each point seemed devalued, equating to approximately 0.2Rs instead of the promised 1Rs. Furthermore, redemption was only possible once the points reached a minimum of 5000. Dissatisfied, I felt the need to master credit card usage further and started exploring other cards with better rewards. A friend recommended the Standard Chartered card, boasting a generous points system. However, I soon realized their billing practices were flawed, putting me at a disadvantage. Though I accumulated a significant number of points, rectifying discrepancies meant spending hours on customer care calls. The frustration grew, leading me to discontinue the Standard Chartered card. To my dismay, even eight years after cancellation, it still appears on my CIBIL report, indicating a small outstanding due that I have no way of rectifying. Such is the lingering pain I experience from this ordeal.

Stage 5 : Lessons Learned: The Turbulent Journey of Credit Card Ownership

After my wedding, I embarked on my honeymoon in Sikkim, only to be bombarded with incessant calls informing me that I had exceeded my credit card cycle and had outstanding dues. The callers were not only persistent but also incredibly rude. Despite having sufficient funds in my bank account to repay the dues, limited internet access prevented me from making the payment until I returned to Bangalore. Throughout my trip, these relentless phone calls tormented me. Upon my return, I discovered a hefty interest charge imposed on me, prompting me to settle the outstanding amount immediately. It was a relief to clear the debt, but this experience left me questioning the true value of owning a credit card.

The haunting question lingered: Was owning a credit card really worth it? Frustrated by the ordeal, I made the decision to stop using my credit card except for emergencies, as it had no annual fee attached. The incident served as a wake-up call, reminding me of the potential pitfalls and challenges that come with credit card ownership. While credit cards offer convenience and financial flexibility, the harsh reality of unexpected situations and the ruthless tactics of some creditors made me question the overall benefit of relying on them.

I thought I was smart but they over smarted me !!!

Stage 6 : From Credit Card Woes to UPI: The Quest for Simplicity and Fair Deals

After discontinuing the use of credit cards, I encountered an awkward situation while shopping on Amazon. Without an Amazon Pay credit card, I was subjected to a 5% premium on purchases. It felt unfair, as they were inflating the prices to accommodate offers, leaving non-credit card users at a disadvantage. Determined to secure better deals, I decided to apply for an Amazon Pay ICICI credit card, making sure to repay the billed amount instantly, keeping it at 0 INR.

However, to my surprise, when I purchased similar products from local shops and nearby supermarkets, they offered direct discounts on the maximum retail price (MRP). In some cases, these discounts were equal to or even greater than the 5% discount I obtained on Amazon using the Amazon Pay card!

This eye-opening realization led me to bid farewell to credit cards altogether, embracing the simplicity and transparency of UPI (Unified Payments Interface). With UPI, I found a more straightforward payment method that allowed for seamless transactions without the burden of credit card woes. This transition not only freed me from the uncertainties and frustrations associated with credit cards but also presented an opportunity to support local businesses while enjoying fair deals.

Conclusion.

The credit card industry often lures individuals into becoming customers, but once caught in their trap, it’s easy to develop spending habits that lead to debt, jeopardizing financial independence and future retirement savings. While credit cards offer convenience and perks, they can also entice users to overspend and accumulate debt, hindering long-term financial stability. It’s crucial to approach credit card usage with caution, understanding the potential risks and maintaining a disciplined approach to avoid falling into a cycle of debt that could hinder one’s financial goals and retirement plans.

Some Food for Thoughts.

The average number of credit cards per person in the U.S. is 3.8

Studies show that shoppers with credit cards are willing to spend more on items, check out with bigger baskets, and focus on and remember more product benefits rather than costs.

Annual interest rates on credit cards may range between 30% and 45%.

A November 2022 LendingTree survey found that just 35% of cardholders say they always pay their credit card balance in full every month, while 65% say they carry a balance at least some of the time.

Here’s the Comprehensive List of Our Blogs: Keep it Handy, Share with Friends and Family, Smash that Like Button, and Subscribe to Receive Blog Updates First. Your support fuels our passion for creating insightful content!

Disclaimer: This blog post is intended for informational purposes only and should not be considered as financial advice. Always conduct thorough research and consult with a qualified financial professional before making investment decision.